SpaceX’s long-awaited market debut on June 12 brought in $75 billion at $135 per share, pushing the company’s valuation past $2 trillion and making its founder, Elon Musk, the first person on Earth to hold a trillion-dollar fortune.

But Musk wasn’t the only one cashing in. Investors who purchased shares at the offering price saw returns of approximately 20% in a matter of hours, while those who backed the company in its early private rounds enjoyed even more dramatic profits.

Crypto participants, on the other hand, were completely shut out of the event. They were left holding pre-IPO subscription tokens on exchanges like Binance, Bybit, and Bitget, with no SpaceX shares allocated to them whatsoever.

As SPCX stock climbed, major tokenized equity systems fell apart. Middlemen couldn’t lock in share allocations, token launches were suddenly scrapped, and platforms rushed to process refunds and manage the fallout.

In essence, the episode served as a real-world stress test for the idea of “tokenized IPO access.” The pricing mechanism functioned as expected, but actual delivery of the underlying shares did not.

Pre-IPO perpetuals as a parallel price signal

Data from Talos Research, shared with Cointelegraph on June 15, showed that in the half hour before Nasdaq trading began, SPCX perpetual contracts traded at a volume-weighted average price (VWAP) of $159.89 across Hyperliquid, Binance, and OKX — roughly 6.6% above the opening price. Meanwhile, Cerebras (CBRS) perpetuals on Hyperliquid came within 1.3% of the Nasdaq open.

It’s also worth highlighting that SPCX perps surged past $220 in mid-May before steadily drifting downward toward the IPO date as traders adjusted their expectations to more realistic valuation levels, according to Talos Research.

SpaceX aggregated VWAP across venues, May 17 – June 8. Source: Talos

Pre-IPO perpetual contracts on derivatives platforms demonstrated that onchain traders could produce reliable price discovery and deep liquidity for a high-profile tech unicorn before a single share officially traded. These instruments offered a live snapshot of where speculators believed the stock would land by the time the opening bell rang.

Related Crypto Biz: SpaceX fuels tokenization’s next boom

“These signals will become increasingly hard for underwriters and consumer-facing platforms to overlook,” Samar Sen, head of international markets at Talos, told Cointelegraph, “especially for marquee listings where there’s already intense global interest before the IPO even launches.”

He added that these markets could “serve as a valuable supplementary data point alongside institutional order books, private market pricing, and peer-company comparisons.”

Why tokenized SpaceX “IPO access” fell apart at the finish line

The issue, then, wasn’t with synthetic, futures-style exposure to SpaceX’s valuation. Pre-IPO perpetuals “performed as designed,” Sen explained, proving themselves to be “a venue for continuous trading and price discovery ahead of the listing.”

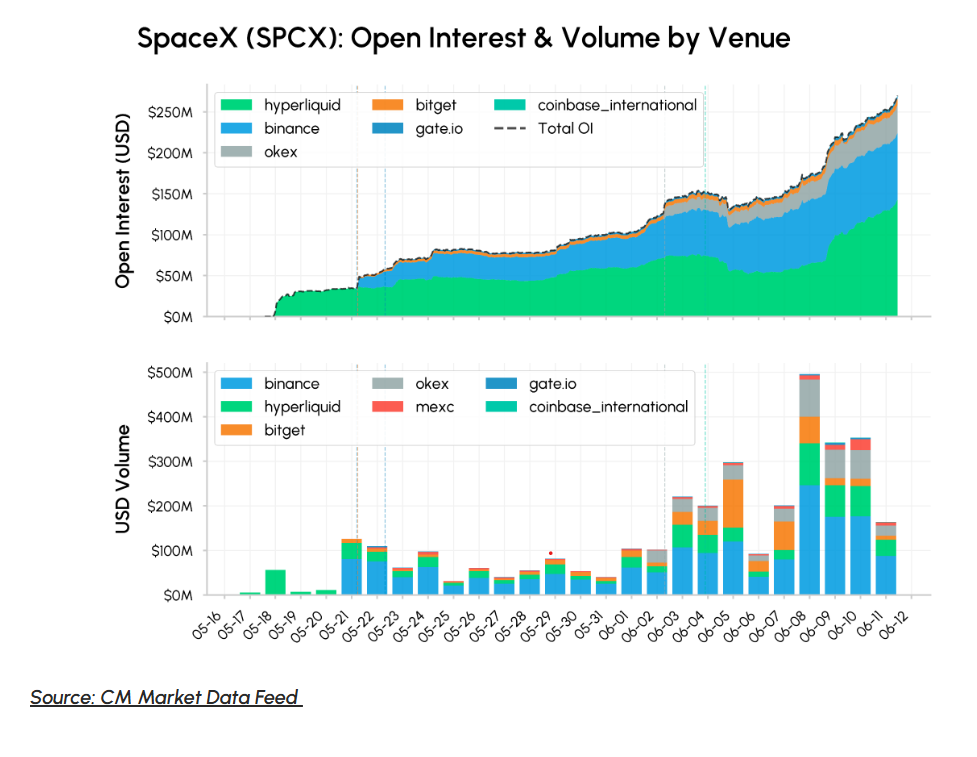

Talos Research data indicated that SPCX perpetual markets logged approximately $4.6 billion in trading volume on IPO day, with total open interest reaching nearly $500 million across eight platforms, including Hyperliquid, Binance, OKX, and Kraken. Cerebras (CBRS) on Hyperliquid recorded $281 million in volume on its IPO day.

Perpetual traders were able to profit from both the pre-IPO price swings and the post-listing convergence. But investors who had purchased tokenized claims on SpaceX IPO shares missed out on the gains entirely.

The SpaceX IPO was oversubscribed four times over, meaning many retail investors received too few shares, tiny partial fills, or no allocation at all.

SpaceX open interest by volume and venue, May 16 – June 12. Source: Talos

SpaceX-linked tokenized shares on major exchanges collapsed at the final stage, with platforms like Binance, Bybit, and Bitget Wallet all scrapping their campaigns and processing refunds after xStocks failed to deliver the underlying share allocation.

Alvin Kan, chief operating officer of Bitget Wallet, told Cointelegraph that users had signed up to participate in a tokenized IPO offering facilitated through Kraken’s xStocks, and that the tokens, “if issued,” would have represented economic exposure to SpaceX shares.

Related: Bybit to offer tokenized SpaceX IPO access through xStocks

The tokens never materialized. Kraken couldn’t meet demand from its own user base, let alone act as a distribution channel for third-party platforms, since the bottleneck came from the availability of actual IPO shares — not from any failure in the onchain infrastructure itself.

How exchanges reacted when the allocation pipeline ruptured

Users were left with nothing as platforms released notices citing “circumstances beyond” their control, forcing them to cancel their campaigns and return subscribed funds.

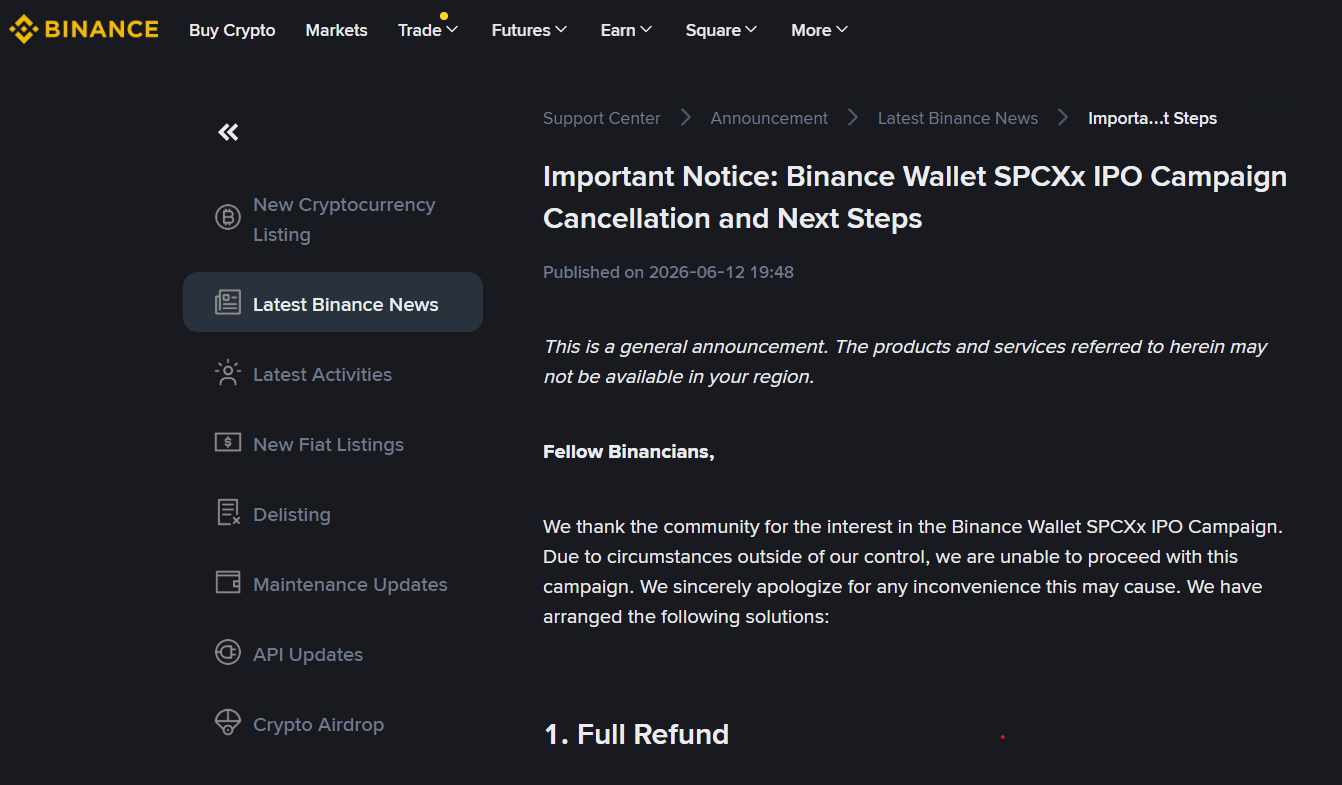

Binance founder and former CEO Changpeng Zhao shared the notice on X with the remark, “Protect users when things don’t go as planned,” which unleashed a torrent of angry responses from retail traders.

Binance customer notice, SpaceX IPO campaign cancellation. Source: Binance

One user wrote, “last in the queue, again,” and pointed to the $557 million in crypto capital raised across “three of the world’s largest exchanges” to buy tokenized SpaceX shares.

“All cancelled. Zero shares delivered… Turns out you still need the underlying asset. Blockchain doesn’t magically conjure shares into existence when Wall Street decides who gets the allocation.”

A Binance Wallet spokesperson told Cointelegraph that its involvement in the campaign was restricted to technical and support services. Binance Wallet was not responsible for “pricing, issuance, backing, or redemption,” they stated, and user-facing materials clearly noted that allocation was not guaranteed.

Despite also being caught in the xStocks bottleneck, Bitget — after canceling its pre-market subscriptions and refunding users — pivoted to Reality, a real-world asset platform supported by the exchange.

Related: Kraken offers SpaceX IPO access through xStocks

Bitget CEO Gracy Chen told Cointelegraph that Reality offers 1:1 tokenized SpaceX shares (rSPCX) on the spot market, held with a broker, replacing the exchange’s third-party xStocks initiative.

She explained that for users, this means access to “properly backed” US equities, rather than short-term structures chasing a single hyped IPO.

The gap between onchain exposure and real allocations

At the core of the SpaceX debacle lies a straightforward structural disconnect. Crypto platforms can create synthetic or tokenized exposure to a stock, but they have no control over primary market allocations, which are only accessible through underwriters with broker-dealer networks.

Pre-IPO perpetuals delivered a powerful real-time signal of where traders believed SPCX should trade, but the tokenized IPO campaigns relied on a single upstream allocation channel that ultimately ran dry.

Sen argued this is precisely why pre-IPO derivatives should be viewed as “signals” rather than replacements for the IPO machinery itself, and the SpaceX episode underscores the “need for greater caution around how different forms of pre-IPO exposure are structured, marketed, and understood.”

Kan said the episode points

You are a paraphrasing software that takes an article in HTML format and rewrite it in a way that is easy to read and understand, Keep HTML as-is, change the text as far as you can. Do not change the content language: to a “broader reality facing the tokenized RWA space,” adding that onchain infrastructure for distribution and settlement is ready, but the mechanisms for crypto-native channels to access primary market allocation are still developing.

Retail demand, he said, is growing faster than the supply-side infrastructure, and closing that gap will require “closer collaboration between crypto platforms, traditional intermediaries and regulators.”

Tokenization can improve access, but it can’t create shares

The legal constraints also help explain why the SpaceX IPO was never going to happen onchain in the first place.

Brogan Law’s Aaron Brogan noted that a token sold to raise $75 billion for SpaceX and marketed on the company’s future performance would fall squarely on the securities side of the Securities and Exchange Commission’s (SEC) recent token guidance line.

Related: SEC plan to scrap ‘Rule 611’ positive for tokenized US stocks: Galaxy

Between securities law, tax uncertainty and the scrutiny a mega-deal would invite, he argued, “there is no path to do so reliably,” making a full-blown token sale an unrealistic substitute for a traditional IPO for a company of SpaceX’s size.

A spokesperson from the SEC declined to comment on whether the regulator had concerns around crypto platforms’ promotion of IPO access or whether securities regulations adequately address tokenized equity offerings.

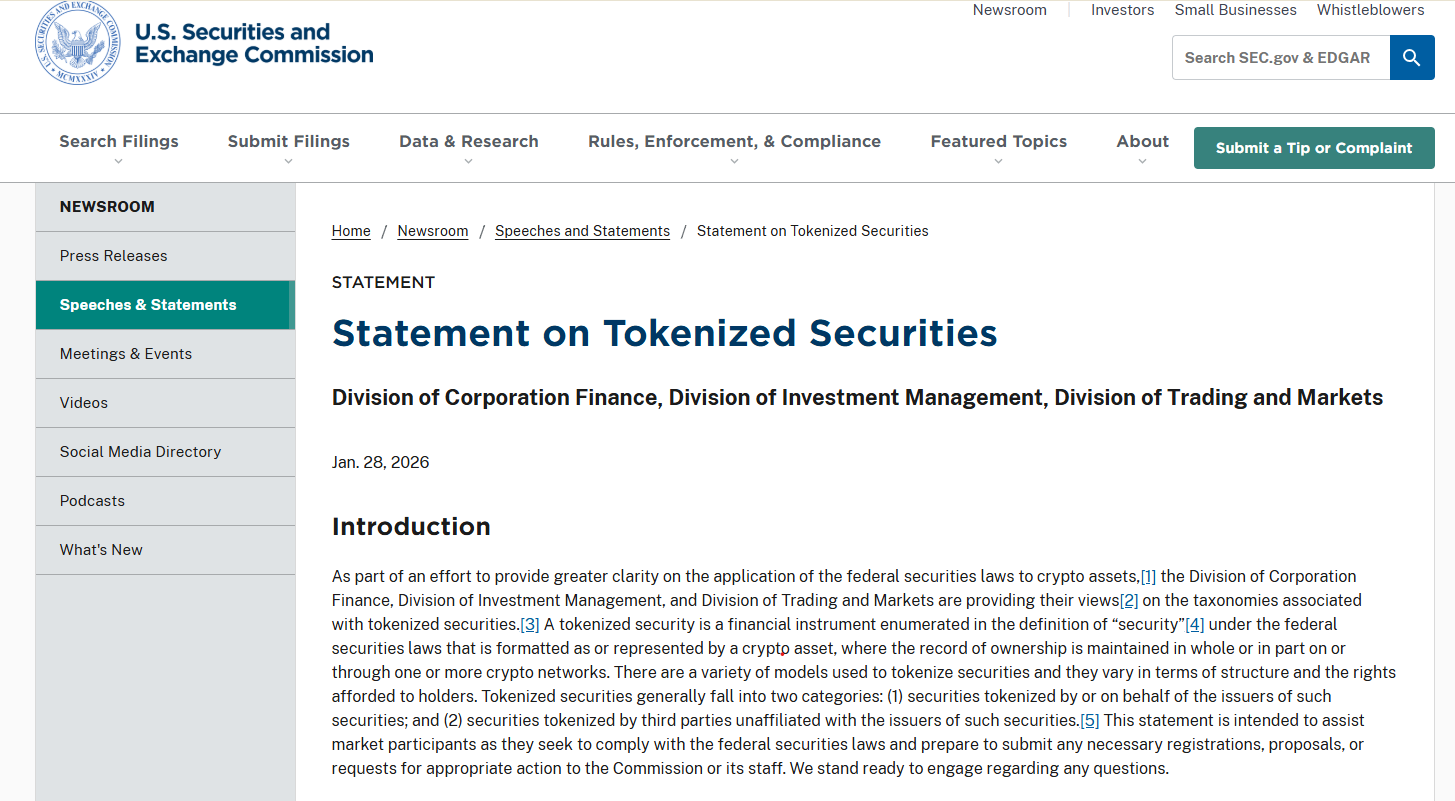

Statement on Tokenized Securities. Source: SEC

In a January 2026 staff statement on tokenized securities, however, the SEC stressed that tokenized stocks remain full securities subject to registration and disclosure rules, explicitly distinguishing between custodial, issuer-sponsored tokenization and synthetic or third-party wrappers.

The future of tokenized IPO access

For all the drama around the SpaceX IPO, none of the key players believe it has killed the tokenized equity story, but rather sharpened the conditions under which it can work.

Dinari, a tokenized equities platform whose tokenized $SPCX maintained continuous uptime as the allocation pipe ran dry, chief executive Gabriel Otte told Cointelegraph the long-term opportunity is to “extend the reach of public markets, not reinvent them.”

He said that was achievable by starting with real underlying securities, regulated custody and clear legal rights, then using tokenization to improve access and settlement rather than to sidestep the rules.

Chen, for her part, said the exchange has learned to avoid short-term, third-party structures and instead build 1:1, broker-backed tokens it can stand behind.

For Brogan, the SpaceX IPO exposed the difference between pricing a stock and allocating one. Crypto markets were able to generate liquidity and price discovery ahead of the listing, but access to actual IPO shares remained firmly in the hands of traditional market participants.

Sen concluded that, while investors may be more cautious about products promising exposure to underlying private company shares, the scale of activity surrounding SpaceX shows these markets are “becoming increasingly difficult to ignore.”

Magazine: How to fix suspected insider trading on Polymarket and Kalshi