If you’ve been steadily investing in the C and S Funds, well done. With the S&P 500 recently surging beyond 7,200 and setting new records, your TSP balance has probably never looked stronger.

Those gains are well deserved. But now is the moment to guard them. There’s a harsh reality about Wall Street that every investor eventually confronts:

Unrealized gains don’t count until you actually secure them.

At the moment, the C and S funds are performing well since they track the stock market, which continues to climb. But keeping every dollar of profit allocated there is like winning big at a roulette table and then putting it all on the next roll.

Despite the impressive surface numbers, experienced investors are already bracing for what lies ahead. They recognize how shaky the broader economy remains, and beneath the surface there’s not one, but four serious red flags waving.

The Warren Buffett Indicator

Warren Buffett’s most trusted market gauge is a straightforward formula that compares the total worth of the U.S. stock market against the nation’s overall GDP. This metric gets a lot of attention because it addresses a core question: Is the stock market rising because the underlying economy is genuinely expanding, or is it merely driven by inflated speculation?

In the past, a ratio near 100 suggests the stock market is reasonably priced and accurately mirrors the real economy. Economists broadly consider a reading of 200 to be entering risky territory. Right now, the Buffett Indicator has hit an unprecedented peak of 234.

To provide some context, at the very height of the 2000 Dot-Com bubble, just before a crash destroyed trillions of dollars in retirement savings, the indicator only climbed to about 160. A reading of 234 signals that the market is dramatically overvalued at this point.

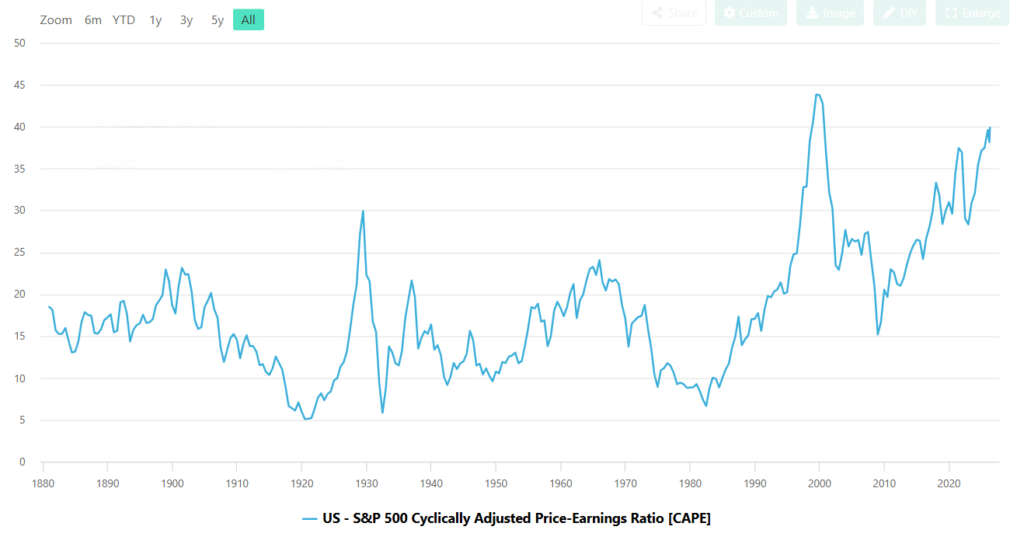

The CAPE Ratio

The Cyclically Adjusted Price-to-Earnings (CAPE) ratio measures how expensive stocks are by examining inflation-adjusted corporate profits averaged across the past decade. This metric matters because it filters out short-term earnings surges and the effects of corporate stock buybacks, revealing the genuine long-term valuation of the market. Historically, this ratio has hovered around 17.

Today, the CAPE ratio sits at an eye-popping 39.89. Across the entire history of the U.S. stock market, valuations have only reached such extreme levels twice: during the late-1990s technology bubble, and the post-COVID stimulus surge of 2021.

Both of those episodes were followed by brutal, extended market downturns that erased years of retirement wealth for investors who failed to shift their gains in time.

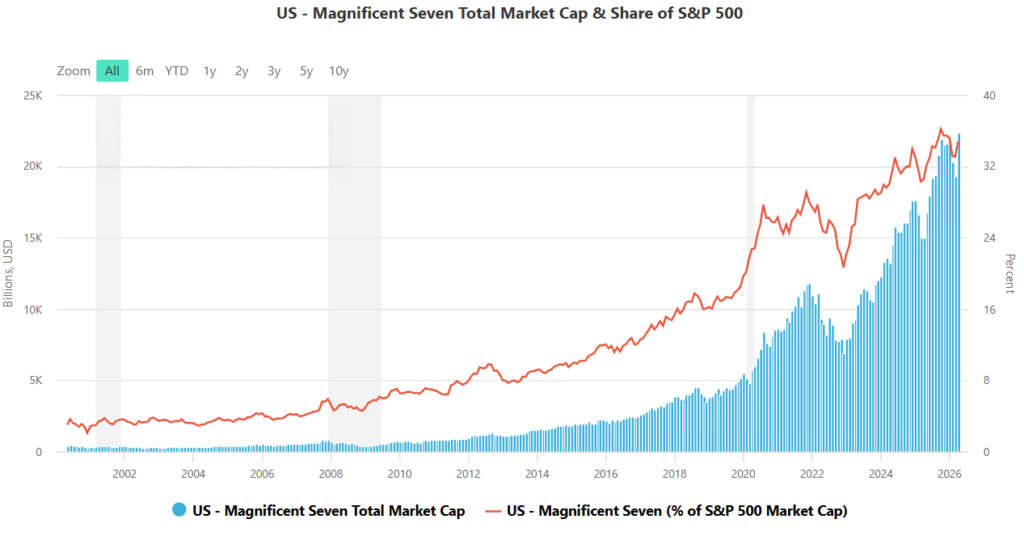

The AI Tech Bubble

When you glance at the S&P 500, it appears as though the entire business world is thriving. But that’s misleading. Recent market advances are overwhelmingly driven by a small group of massive technology firms pouring billions into Artificial Intelligence infrastructure.

While these companies are generating profits, their share prices have soared far beyond what many analysts believe their current earnings can realistically support. Their sky-high valuations are being sustained by hundreds of billions of dollars flowing into AI infrastructure, powered by the expectation that it will eventually produce enough returns to match the excitement.

This concentration is so severe that even top banking officials and tech industry leaders are raising the alarm, openly warning that the situation increasingly resembles a bubble. In practical terms, disappointing earnings from any of these tech giants could burst the bubble and send the rest of the market tumbling like a row of falling dominoes.

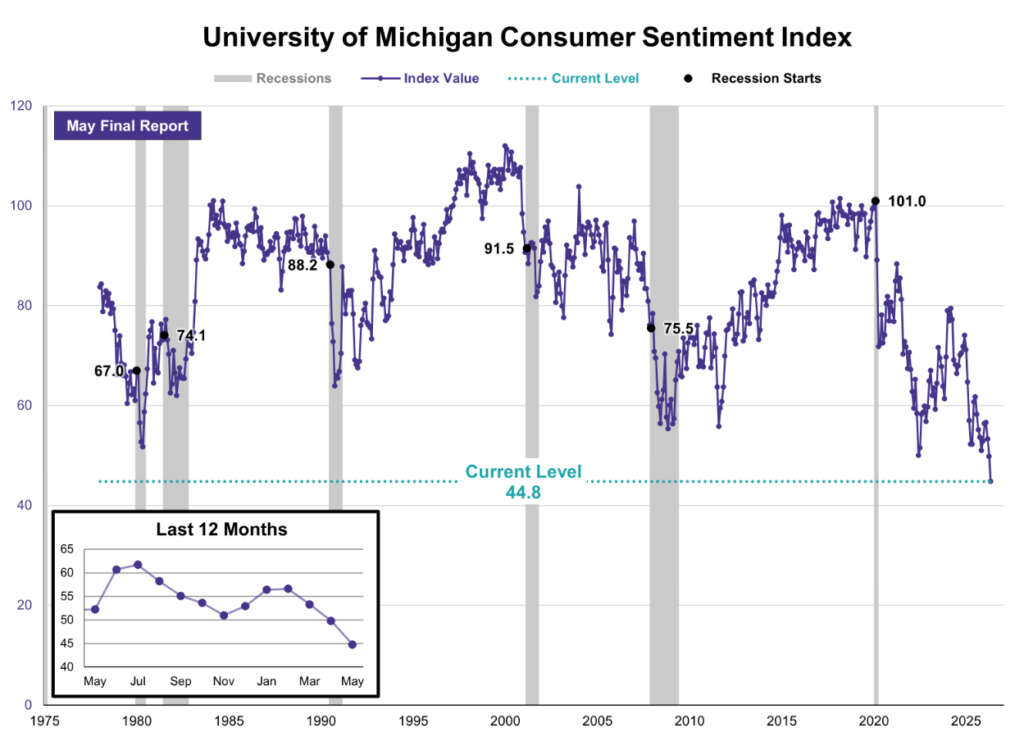

The Consumer Sentiment Index

Lastly, there’s a glaring gap between the prosperity on Wall Street and the reality on Main Street. Even as the stock market continues to set records, consumer confidence is plummeting. Everyday Americans are being squeezed by persistent inflation, rapidly rising debt, and steep borrowing costs.

In fact, the University of Michigan’s renowned Consumer Sentiment survey just logged its lowest reading in more than 50 years of tracking. Put simply, never before in modern times have Americans felt more pessimistic about where the economy is headed.

In the past, the stock market hasn’t been able to ignore economic reality for long when everyday consumers are stretched financially thin. Since consumer spending drives about 70% of the country’s Gross Domestic Product, a gap this significant usually leads to a painful market adjustment sooner or later.

Securing Your Profits Without Paying Taxes

Past market cycles clearly show the consequences of dismissing these red flags. In 2000, identical warning signals appeared right before the dot-com bubble burst, destroying roughly $5 trillion in household wealth. In 2008, another $7 trillion disappeared. Then in 2020, a sudden liquidity crisis wiped out nearly a third of the market’s value within weeks.

Market crashes rarely send advance notices in the mail. They strike suddenly, erasing years of wealth accumulation before most people have a chance to respond.

Right now, once again, the economy finds itself balancing on a knife’s edge. The continuing conflict in Iran has set off a worldwide oil crisis, driving energy costs up sharply and stoking fears about rising inflation once more. If you step back and look at the big picture, your C Fund and S Fund holdings are much like a roller coaster car slowly grinding to the highest point on the track. A sharp decline is virtually guaranteed.

Protecting your retirement wealth isn’t about trying to pick the precise top of the market—nobody can do that. Instead, it means paying attention to the numbers and knowing when it’s the right moment to secure your gains using a tangible asset.

When signals hit extreme levels, less experienced investors tend to get greedy. They leave all their savings in the stock market, watching it rise on the way up, only to see those gains evaporate when the inevitable downturn arrives.

Experienced investors, on the other hand, shift their profits into real, physical assets.

And because your retirement funds sit inside a Thrift Savings Plan, you can actually transfer those gains into physical assets without paying any taxes.

The Gold “Opportunity” Available to Federal Workers

Most federal employees think their only option for shielding their money from a stock market downturn is to move it into the G-Fund. However, given the persistent inflation we’ve been experiencing, the G-Fund’s modest returns virtually guarantee that your purchasing power erodes over time.

Luckily, there’s a more effective approach.

An often-overlooked provision in the TSP Modernization Act gives federal workers over age 59½, as well as those who’ve already retired, access to an alternative beyond the high-risk C Fund or the inflation-eroding G Fund.

By law, you’re permitted to execute a tax-free, penalty-free rollover that transfers part of your TSP balance into a Gold IRA.

This process lets you convert paper gains into tangible, government-issued precious metals, such as American Gold Eagles produced by the U.S. Mint.

By reallocating a portion of your portfolio into gold, you permanently lock in your profits.

You’re also creating a hedge against both inflation and market volatility for your retirement, all while preserving the tax benefits of your traditional retirement account.

For More Information

Financial advisors who earn commissions from keeping your money in C and S Fund mutual funds won’t suggest shifting your profits into physical metals—especially since they collect their fees whether the market rises or falls.

For this reason, National Gold Group has put together a complimentary guide designed specifically for federal workers and retirees, titled “The TSP-to-Gold Guide.”

Within this free resource, you’ll learn:

- The “TSP-to-Gold” Method: A detailed three-step rollover process showing exactly how to move part of your funds without triggering IRS penalties, tax liabilities, or common costly errors.

- The “Crisis Shield” Breakdown: A clear, visual explanation of how gold performs during steep market downturns, liquidity crises, and stretches of high inflation.

- The “Peace of Mind” Safeguard Plan: How to use your TSP balance to acquire government-backed physical gold, confirm your metals are stored in IRS-approved facilities, and steer clear of expensive ongoing IRA charges.

- The “Total Control” Withdrawal Strategy: How to keep maximum flexibility, including options for taking physical possession of your metals or selling them for cash, so you retain full authority over your retirement distributions without being hit by surprise fees.

You’ve worked hard to accumulate those TSP profits. Now it’s time to safeguard them with something that’s solid and real.

>> Get your complimentary guide here.

Copyright

© 2026 Federal News Network. All rights reserved. This website is not intended for users located within the European Economic Area.