In brief

- ChatGPT can now link to over 12,000 banks and financial services through Plaid, allowing it to view your account balances, transaction history, and active subscriptions.

- The feature is launching in preview for ChatGPT Pro users in the U.S. and uses GPT-5.5 Thinking, OpenAI’s most advanced reasoning model.

- OpenAI purchased two AI finance startups in the past year—Roi and Hiro—to help build this capability.

For years, ChatGPT has offered general budgeting tips. You’ve heard it all before: keep track of your subscriptions, set up automatic savings, and try cooking at home more often.

But some users wanted something more tailored—for whatever reason.

If you’re one of those users, OpenAI has just introduced a personal finance feature in ChatGPT that connects directly to your bank accounts and answers money-related questions based on your actual spending habits—not national averages. It’s rolling out first to Pro subscribers ($200/month) in the U.S. on web and iOS.

The feature relies on Plaid, the financial data platform that already supports Venmo, Robinhood, and thousands of other fintech applications. Once connected, ChatGPT gains read-only access to your balances, transactions, investments, and debts across more than 12,000 institutions—including Chase, Fidelity, Schwab, American Express, and Capital One.

It can’t move money or view your full account numbers—it simply reads all your financial data, giving it the ability to build a complete financial profile of who you are. That’s all, nothing to worry about… right?

The difference in results is dramatic. Without your accounts linked, ChatGPT responds to “help me save more” with a generic set of suggestions: cancel subscriptions, eat out less, automate transfers, and so on. With your accounts connected, it analyzes your last 90 days of real spending across dining, shopping, and transportation—and creates a personalized monthly budget with specific dollar amounts based on your actual habits.

If you wanted more personalized advice from the standard version of ChatGPT, you’d have to manually download your bank statements one at a time and upload all that data—a time-consuming process.

This new feature automatically retrieves

everything for you.

This decision wasn’t made in a vacuum. Just last month, OpenAI purchased Hiro Finance—a fintech startup that had positioned itself as an “AI personal CFO.” The acquisition was essentially an acqui-hire, meaning the Hiro team was absorbed into OpenAI while Hiro’s own product was discontinued. This marked OpenAI’s second fintech purchase in under a year, after it previously acquired Roi, a personalized investing application.

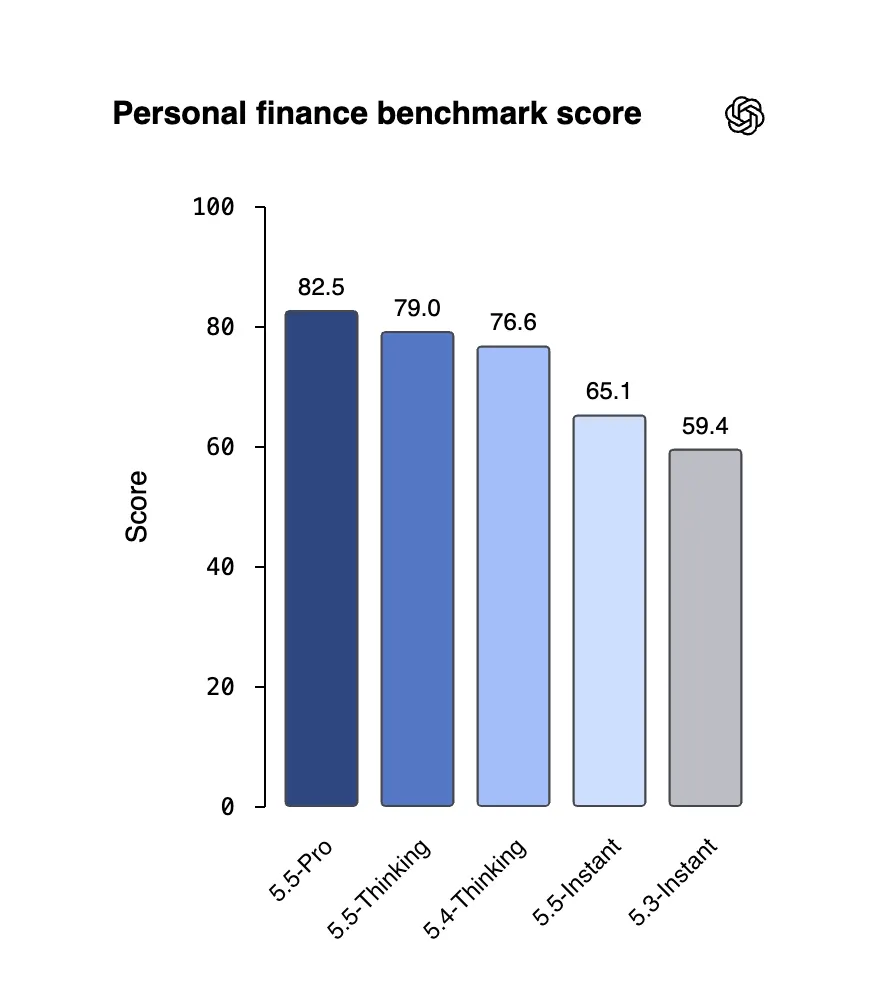

The new feature also establishes its own financial performance standard. OpenAI collaborated with more than 50 finance professionals to assess how well its models handle complex personal finance tasks. GPT-5.5 Thinking—the default model powering the Finances feature—achieved a score of 79 out of 100 on that benchmark. GPT-5.5 Pro, which is available to Pro subscribers, scored 82.5.

OpenAI isn’t the only player entering this space. Perplexity recently rolled out its own finance product connected through Plaid, and Intuit is expected to integrate with ChatGPT soon—enabling capabilities like estimating the tax consequences of selling stock or gauging the likelihood of credit card approval, all within the chat interface.

But why?

The obvious concern: Is it really safe to share this much financial information with a chatbot?

Plaid employs bank-level encryption, doesn’t retain your bank login credentials, and has facilitated over 150 million connections across more than 12,000 institutions without experiencing a major security breach. The security backbone here is Plaid. The more pressing question is what OpenAI does with your data once it reaches their systems.

“Your conversations involving connected financial accounts follow the same model training settings you’ve chosen across ChatGPT,” the policy states—so if you’ve opted out of contributing to model training, that preference applies here as well. You can also disconnect your accounts at any time, and OpenAI says synced data is removed from its systems within 30 days.

One critical limitation OpenAI is upfront about: This tool is not a financial advisor. It can identify patterns and recommend targets, but it carries no fiduciary duty—meaning no legal obligation to act in your best interest, so any mistakes you make are entirely your own. That’s a significant constraint that banks and regulators will likely examine closely as the product rolls out beyond Pro users.

OpenAI followed the same playbook in healthcare earlier this year, launching a specialized version of ChatGPT for clinicians without actually accepting responsibility for the clinical guidance it provides.

Personal finance is simply the next industry in this same strategy: take a field where people already use ChatGPT informally, layer in structured data access, and release a purpose-built vertical product. OpenAI noted that over 200 million people already ask ChatGPT financial questions every month; the new feature is simply catching up to how people are already using the platform.

The expansion to Plus users will follow after OpenAI gathers feedback from the Pro preview. Those without a paid subscription can always take the DIY approach: a capable Hermes agent paired with a strong model (ideally a local model or a privacy-focused provider like Venice) and some manual data input should deliver roughly comparable results. It’s less convenient, but your data remains entirely under your control.

Daily Debrief Newsletter

Start every day with the top news stories right now, plus original features, a podcast, videos and more.