By Marc Kavinsky, Lead Editor at IoT Business News.

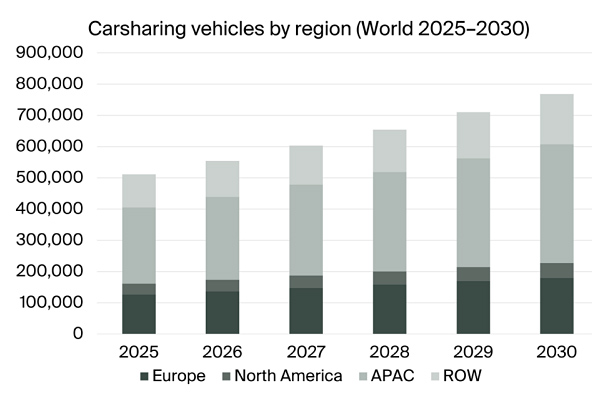

According to Berg Insight, the worldwide public carsharing fleet is set to expand from 511,000 vehicles at the close of 2025 to 768,000 by 2030, while the number of users is projected to climb to 141.1 million during the same timeframe. This outlook highlights the growing importance of telematics, reservation systems, and fleet management software as essential infrastructure for shared mobility services.

While shared mobility is frequently viewed through the lens of consumer transportation trends, its day-to-day operations resemble a distributed IoT enterprise: thousands of vehicles left unattended, diverse access methods, remote user verification, automated billing, real-time vehicle condition tracking, and ongoing fleet efficiency improvements. Without connected vehicle hardware and integrated software platforms, scaling the modern carsharing model would be nearly impossible.

This is the key takeaway from Berg Insight’s most recent forecast. The research firm estimates that the number of vehicles in public carsharing services will grow at a compound annual rate of 8.5 percent, rising from 511,000 at the end of 2025 to 768,000 by the end of 2030. The user base is anticipated to expand at a slightly quicker pace, increasing from 91.0 million people in 2025 to 141.1 million in 2030, which corresponds to a CAGR of 9.2 percent.

The forecast also sheds light on the regional distribution of the market. Asia-Pacific holds the largest proportion of carsharing vehicles, with Europe coming in second. Europe is particularly notable for another reason: free-floating carsharing is the dominant operational model there, both in terms of membership numbers and fleet size, as reported by Berg Insight.

Why this forecast stands apart from a typical mobility growth narrative

The real significance of this report goes beyond the fact that carsharing is growing. The more critical insight is that this expansion is closely linked to increasingly sophisticated connected fleet infrastructure. Berg Insight does not portray carsharing as a market shaped solely by vehicle availability or consumer interest; instead, it presents it as an ecosystem reliant on in-vehicle telematics, booking management, billing systems, fleet oversight, dashboards, and analytics.

This distinction is crucial for IoT suppliers. A station-based round-trip service and a free-floating urban fleet impose very different requirements on platforms. Station-based carsharing can depend on fixed drop-off locations and more predictable vehicle flows. Free-floating services, on the other hand, demand that operators manage vehicle availability across a defined service area, track usage rates, and support more agile operational decisions. While the press release does not detail the technical specifics, the message is clear: as free-floating models become more prominent in certain regions, software and telematics capabilities become increasingly vital to service dependability.

Not all carsharing operators develop this technology in-house. Berg Insight points out that some rely on proprietary hardware and software, while many turn to specialized vendors for products and services. The market encompasses suppliers that deliver complete, end-to-end solutions combining telematics hardware and carsharing platforms, as well as companies that focus exclusively on either hardware or software. Notable vendors in this space include Invers, Vulog, Convadis, Targa Telematics, Optimum by Shiftmove, Mobility Tech Green, WeGo Carsharing, Atom Mobility, CT Mobility, Cantamen, MOQO, 2hire, Bosch, and Astus.

For OEMs and vehicle technology providers, this presents a real integration challenge. Carsharing vehicles are not merely connected cars added to a rental fleet. They must enable unattended access, support booking workflows, facilitate usage-based billing, and allow for continuous operational monitoring. The more diverse the fleet or the more varied the service model, the stronger the need for seamless interoperability between embedded hardware, mobility software, and back-office systems.

Profitability is transforming the connected mobility technology stack

Berg Insight also notes that many operators have shifted their priorities in recent years, moving away from chasing market share and toward improving profitability and boosting vehicle utilization rates. This shift carries significant implications for technology providers, because utilization-focused operations demand deeper insight into fleet status, demand trends, and asset performance. In this context, telematics data is no longer a supplementary feature; it becomes a core component of the business model.

The corporate carsharing segment introduces yet another layer. Berg Insight estimates that corporate carsharing accounted for 154,000 vehicles at the end of 2025 and is expected to reach approximately 250,000 vehicles by 2030. For businesses, leasing companies, and system integrators, this signals sustained demand for shared fleet solutions that can minimize manual administration while enabling controlled access and usage tracking across corporate users.

The operator landscape remains diverse. Specialist providers such as Times Car, Socar, Communauto, Evo Car Share, Miles, Stadtmobil, Cambio, MyWheels, Greenwheels, Enjoy, Mobility Cooperative, Citiz, Traficar, TikTak, Turbi, and GoGet operate alongside car rental groups including Sixt Share, Zipcar, ORIX CarShare, and G Car. Carmaker-backed services include Free2move, Kinto Share, and Wible. Berg Insight adds that the top 30 carsharing service providers represent roughly 63 percent of total members and manage about 56 percent of the global fleet.

For connectivity providers, the opportunity extends well beyond SIM cards or data plans. Carsharing fleets require reliable connectivity as part of a broader service architecture encompassing vehicle access, fleet visibility, and operational control. For IoT platform vendors and integrators, the industry’s shift toward utilization and profitability may matter more than headline fleet growth: operators will need tools that help them reduce the number of idle vehicles, not simply connect more of them.