By Marc Kavinsky, Lead Editor at IoT Business News.

The global installed base of cellular-connected POS terminals is set to grow from 184 million units in 2025 to 247 million by 2029, as connectivity becomes a standard design requirement rather than an optional feature in retail infrastructure.

The evolution of payment infrastructure is increasingly shaped by connectivity constraints rather than software capabilities. In fragmented retail environments—ranging from urban micro-stores to mobile service operations—the ability to deploy and operate terminals without relying on fixed-line infrastructure has become a decisive factor.

In this context, cellular connectivity is no longer a premium add-on. It is becoming the default deployment model for a growing share of point-of-sale (POS) devices.

According to new data from Berg Insight, 53 percent of POS terminals shipped globally in 2025 included cellular connectivity. This shift translates into a rapidly expanding installed base, projected to grow at a CAGR of 7.6 percent to reach 247 million units by 2029.

From optional feature to baseline requirement

What stands out in these projections is not just growth, but standardization. Once cellular penetration crosses the 50 percent threshold in shipments, it fundamentally changes how devices are designed, sourced, and managed.

For OEMs, this means integrating cellular modules, antenna systems, and certification processes into core product architectures. For operators and solution providers, it shifts attention toward lifecycle management: provisioning, connectivity orchestration, firmware updates, and long-term support.

In effect, POS terminals are increasingly behaving like managed IoT endpoints rather than static retail equipment.

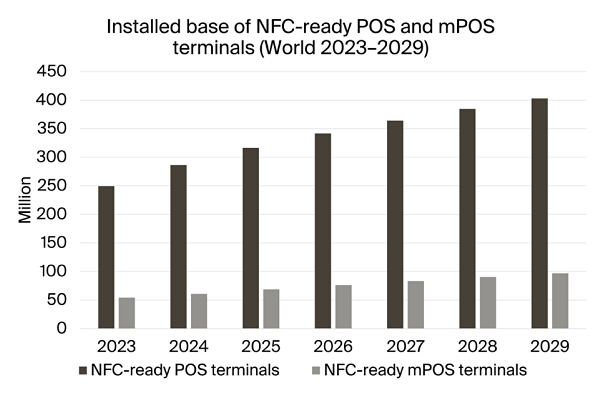

Near-universal NFC adoption simplifies the payment stack

Alongside the rise of cellular, NFC capabilities are approaching full market saturation. Berg Insight forecasts that the global installed base of NFC-ready POS terminals will increase from 316.5 million units in 2025 to 403 million in 2029, representing a CAGR of 6.2 percent.

By the end of the forecast period, more than 97 percent of all POS terminals are expected to support NFC, up from 92 percent in 2025.

This near-universal adoption reduces fragmentation in payment acceptance, enabling application providers and payment ecosystems to standardize around contactless interactions across regions and device types. It also reinforces a broader industry shift toward faster, low-friction transaction models.

Android POS gains ground as software becomes the differentiator

Another structural shift highlighted in the report is the rapid adoption of Android-based POS terminals. Close to half of all devices shipped in 2025 were Android-based, reflecting a broader industry move toward open, app-centric platforms.

“The Android POS terminal category has become very popular lately. Close to half of the POS terminals sold in 2025 were Android POS terminals.”

While Android simplifies application development and ecosystem integration, it also raises the bar for device management. Security patching, policy enforcement, and application lifecycle control become continuous operational requirements rather than occasional interventions.

For vendors, differentiation is increasingly moving away from hardware capabilities toward software ecosystems, security frameworks, and fleet management efficiency.

mPOS growth continues—but SoftPOS introduces a structural shift

The mobile POS (mPOS) segment is expanding at a similar pace to traditional terminals. The installed base reached 84.9 million units in 2025, with NFC-enabled devices accounting for 81 percent of that total.

By 2029, NFC penetration in mPOS is expected to reach 93 percent, supported by an 8.9 percent CAGR in NFC-ready devices.

However, a parallel trend is beginning to reshape the competitive landscape: the rise of SoftPOS solutions.

“The mPOS device segment has also started to face competition from SoftPOS solutions which allow businesses to accept payments via standard iOS or Android devices.”

Although still relatively limited in scale—fewer than 15 million smartphones are currently used for SoftPOS—this model challenges the traditional hardware-centric approach to payment acceptance.

A dual model for payment acceptance is emerging

Taken together, these trends point toward the emergence of two distinct operational models:

- Dedicated POS terminals, increasingly connected via cellular and managed as IoT fleets, offering controlled environments and high reliability.

- Software-based acceptance (SoftPOS), leveraging general-purpose smartphones, with greater flexibility but less control over hardware and lifecycle conditions.

For the IoT ecosystem, this duality introduces new complexity. Connectivity providers, device management platforms, and security frameworks must adapt to environments where the “device” can either be a purpose-built terminal or a consumer-grade smartphone.

Strategic implications for the IoT value chain

For OEMs, the sustained growth of cellular-connected terminals confirms that integrated connectivity will remain a long-term requirement rather than a regional differentiator.

For system integrators, the challenge shifts toward scaling deployments efficiently—ensuring seamless onboarding, remote configuration, and real-time monitoring across large device fleets.

For connectivity providers, POS terminals represent a high-value IoT segment with strict uptime requirements and predictable usage patterns. As the underlying connectivity becomes increasingly commoditized, differentiation will depend on service quality, provisioning efficiency, and lifecycle support capabilities.

Ultimately, the expansion of cellular POS is less about incremental growth and more about structural transformation: payments infrastructure is converging with IoT architecture principles, where connectivity, device management, and software integration are inseparable.