By Marc Kavinsky, Lead Editor at IoT Business News.

According to Berg Insight, the number of connected alcohol detection and monitoring devices in use across North America and Europe hit approximately 560,000 units in 2025. This highlights a specialized segment of the IoT market where adoption is fueled more by regulatory compliance, oversight, and safety needs than by consumer demand for convenience.

Alcohol testing itself isn’t a new concept, but how it’s being managed is evolving. Traditionally, most alcohol detection tools have served as one-time checks—like a breathalyzer test, a vehicle ignition interlock event, or a supervised screening at a specific site. The connected side of this market introduces something new: the ability to monitor remotely, generate automatic reports, and take action when a test is failed, skipped, or shows signs of tampering.

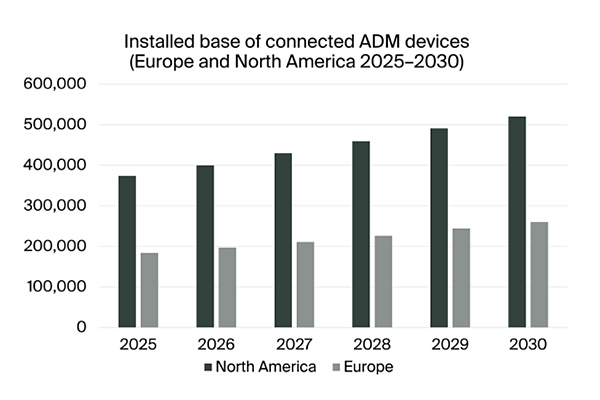

This shift is the backdrop for Berg Insight’s latest findings. The firm reports that in 2025, the installed base of connected alcohol detection and monitoring solutions stood at 374,000 units in North America and 184,000 units in Europe. Looking ahead to 2030, those numbers are projected to climb to 520,000 units in North America and nearly 260,000 units in Europe.

While this market is still small compared to mainstream IoT sectors like fleet tracking or smart metering, it stands out because the need for connectivity is deeply embedded in institutional processes. Berg Insight identifies four primary application areas: road safety and transportation, workplace safety, healthcare and rehabilitation, and legal or public safety. Although these sectors may use similar sensor technologies, they represent distinct markets with different requirements.

An IoT segment driven by compliance

In both regions, ignition interlock devices make up the largest share of connected units, representing about half of the total installed base. These systems are primarily used in programs for individuals convicted of Driving Under the Influence, as well as in workplace fleet safety setups, where a vehicle won’t start unless the driver passes an alcohol test. Other connected device types include breathalyzers linked to smartphones, wearable ankle and wrist monitors, and fixed wall-mounted systems installed at locations like probation offices and workplace entry points.

What sets this market apart from typical IoT industry updates is the underlying driver of demand. This isn’t mainly a story of consumer electronics adoption, nor is it simply about adding internet connectivity to an existing product. Berg Insight points out that the majority of alcohol detection devices sold today are still standalone units with little or no connectivity. The connected segment is therefore a subset of a much older testing market, shaped by government regulations, institutional oversight, and workplace policies rather than by mass-market upgrade cycles.

This distinction is important for IoT vendors. In a consumer breathalyzer, connectivity might be about convenience or personal health tracking. But in offender monitoring, fleet safety, or probation settings, connectivity becomes a core part of the compliance framework. The practical takeaway is that device manufacturers and platform providers need to support event logging, remote oversight, and handling of exceptions—not just collecting sensor data. A missed test or an attempt to tamper with a device carries very different operational consequences than a delayed data reading in a typical monitoring scenario.

Regional variations continue to matter

North America is currently the bigger market. Berg Insight estimates the value of connected ADM solutions there at US$409 million in 2025, with growth expected to reach US$571 million by 2030—a compound annual growth rate of 6.9 percent. In Europe, the market is valued at US$187 million in 2025, projected to rise to US$264 million by 2030.

The regional differences also reflect varying levels of program adoption. Berg Insight notes that only a handful of European countries currently run DUI offender monitoring programs, while relatively few U.S. states mandate real-time connectivity within their ignition interlock programs. This creates an uneven landscape for connectivity growth: the installed base can expand not only through new alcohol monitoring applications but also by transitioning existing offline or intermittently supervised processes to connected platforms.

For original equipment manufacturers, these findings suggest that product design must account for the specific deployment environment. Wearable devices built for continuous monitoring face different challenges than vehicle interlocks or high-throughput stationary testing units. For connectivity providers, the opportunity is unlikely to come from large data volumes; instead, reliability, network coverage, device lifecycle management, and secure data reporting are the key factors. System integrators and public-sector technology partners, on the other hand, may need to link ADM data with case management, fleet safety, or workplace compliance systems.

Berg Insight identifies a range of companies active in this space. North American vendors include Alcohol Countermeasure Systems, Smart Start, Mindr, SCRAM Systems, BI Incorporated, BACtrack, SoberLink, SobrSafe, and Trac Solutions. European providers listed are Draeger, Innovative Process Solutions, Buddi, Dignita, and Senseair. Additional international players mentioned include SuperCom, Breatech, and Autowatch.

The broader significance for the IoT industry is that connected alcohol detection and monitoring sits at the crossroads of sensing, identity verification, policy enforcement, and remote operations. Its growth won’t be determined solely by advances in sensor technology. It will hinge on whether regulators, employers, and institutions decide that real-time or near-real-time alcohol monitoring is essential infrastructure rather than just an optional enhancement to traditional testing methods.