By Marc Kavinsky, Lead Editor at IoT Business News.

According to Berg Insight, the number of water AMI endpoints installed across Europe and North America is set to almost double from 2025 to 2031. This trend signals a clear move away from mobile-based meter reading and toward fixed-network water metering systems.

For water utilities today, the key question is no longer simply whether a meter can transmit data — it’s about how frequently it communicates, which network it uses, and what operational impact that has. While drive-by and walk-by reading methods can digitize the billing process, they fall short when it comes to enabling continuous monitoring, detecting leaks, or delivering near-real-time operational insights.

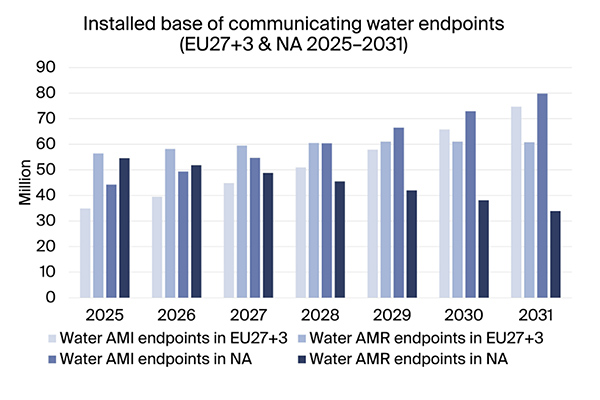

This difference lies at the heart of Berg Insight’s latest market analysis. The research firm estimates that Europe and North America together had 79.1 million water AMI endpoints in place by the close of 2025. That number is projected to grow at a compound annual rate of 11.8 percent, climbing to 154.5 million endpoints by 2031.

Looking at the wider picture, the total installed base of connected utility water meters — covering both AMI and AMR systems — is expected to increase from 190.1 million units in 2025 to 249.2 million units in 2031. AMR meters are those read through mobile methods like drive-by or walk-by collection, whereas AMI meters use fixed network connections and enable a more IoT-driven approach to utility operations.

Why the growing share of AMI is significant

The most telling detail in the forecast isn’t just the overall growth number. Berg Insight’s data shows that AMI made up around 42 percent of all communicating water meters across the two regions in 2025. By 2031, that share is expected to rise to approximately 62 percent. This points to a fundamental shift in the market: utilities aren’t just deploying more connected meters — they’re increasingly choosing fixed-network infrastructure over mobile alternatives.

This is what sets the findings apart from a routine smart metering market report. It draws a clear line between basic meter communication and genuine AMI connectivity, revealing where the market’s center of gravity is heading. For IoT suppliers, this distinction has real consequences for decisions around module selection, network architecture, battery-life planning, data management, and integration with utility platforms.

North America continues to lead as the largest market for both AMR and AMI water metering, according to Berg Insight. Major AMI rollouts in the region started picking up steam about ten years ago, and several projects exceeding 100,000 endpoints have already been completed. Europe ranks as the second-largest market, though its technology environment is more varied and fragmented.

The connectivity landscape is evolving as well. Proprietary solutions and EN 13757-based RF technologies still dominate in both regions, but LoRaWAN and 3GPP-based LPWA standards like NB-IoT and LTE-M are emerging as the fastest-growing technology segments for new water AMI installations. In North America, LTE-M currently stands as the top-growing technology for new deployments. In Europe, LoRaWAN adoption spans a broader geographic footprint, while 3GPP-based LPWA uptake is particularly notable in Spain, where several leading utilities have launched large-scale NB-IoT projects. Strong interest in cellular LPWA is also evident in the UK, Italy, and the Baltic states.

What this means for the IoT ecosystem

For OEMs and meter manufacturers, the forecast underscores the importance of supporting multiple connectivity options rather than approaching water metering as a one-radio-fits-all market. A product strategy tailored to North American LTE-M demand may not translate well to European procurement processes, where LoRaWAN, NB-IoT, EN 13757-based RF, or proprietary systems could all be in play depending on the country and utility.

Connectivity providers face their own set of challenges. Water meters are long-lasting assets, frequently installed in locations that pose difficulties for radio signal propagation — think pits, basements, and underground chambers. While the report doesn’t include specific performance metrics, the rising adoption of LPWA in this sector highlights why deep network coverage, reliable service continuity, and low-power device operation remain top priorities for utilities when making purchasing decisions.

System integrators and enterprises working alongside utilities should also interpret these figures as a sign that data infrastructure will take on greater importance than meter reading alone. AMI deployments generate continuous streams of operational data that need to be woven into billing platforms, customer service systems, leak detection analytics, and asset management tools. The transition from AMR to AMI therefore shifts the complexity away from field collection logistics and toward network operations and software integration.

Berg Insight names Itron, Diehl Metering, Sensus International, Veolia Connected Solutions, and Sagemcom as the companies with the largest accumulated installed bases of water AMI endpoints in Europe as of the end of 2025. In North America, the leading five were Sensus, Badger Meter, Aclara, Neptune Technology Group, and Master Meter. Other vendors active across both regions include Kamstrup, Honeywell, Minol-ZENNER Group, Mueller Systems, Apator, Maddalena, ADD Grup, Janz, Landis+Gyr, and Axioma Metering. SUEZ Digital Solutions is also recognized for its involvement in developing and deploying Wize technology across Europe.

The forecast paints a picture of a water metering market that is becoming increasingly connected, yet far from uniform. For IoT companies, the opportunity is considerable — but the real challenge lies in aligning the right communications architecture with each region’s utility procurement practices, existing installed base, and operational priorities.