Written by Marc Kavinsky, Lead Editor at IoT Business News.

Berg Insight projects that shipments of cellular IoT modules hit 612 million units throughout 2025, with revenues climbing to US$5.6 billion. These numbers signal a market on the rebound, yet they also highlight intensifying strain on module price points and the costs of individual components.

For companies building cellular IoT devices, 2025 was more than just a bounce-back year. It served as a stark reminder that recovering shipment volumes and recovering market value are no longer advancing in sync throughout the module supply chain.

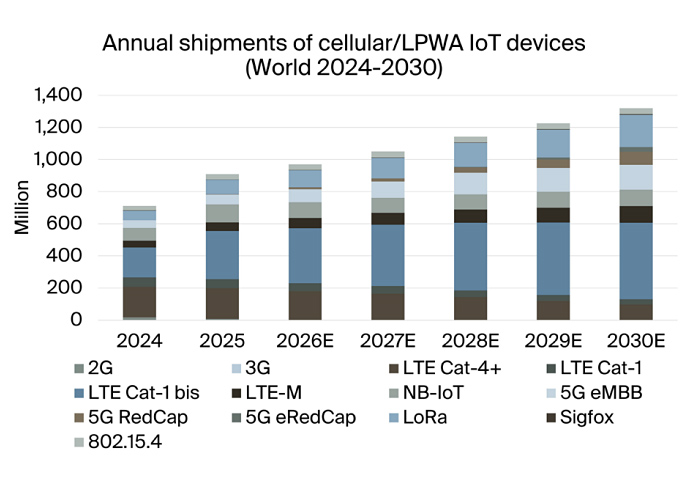

Fresh research from Berg Insight reveals that yearly cellular IoT module shipments stood at 612 million units in 2025, a 33 percent jump compared to the prior year. Revenue grew 19 percent to US$5.6 billion. These numbers leave out automotive NAD modules, which are generally categorized independently owing to their distinct qualification standards, dedicated supply chain structures, and unique pricing models.

The widening gap between shipment growth and revenue growth stands out as a key insight drawn from the report. Drawing from Berg Insight’s data, the average price earned per shipped module fell on an annual basis, even though the market expanded dramatically in unit volume. For original equipment manufacturers and connectivity hardware suppliers, this underscores a market where demand has bounced back, yet the ability to command premium pricing still varies considerably.

Recovery driven by Inventory realignment and national policy shifts

Berg Insight links the resurgence to stronger uptake across every major region following a sluggish stretch that stemmed primarily from bloated customer stock levels. In real-world terms, this means a portion of the 2025 spike is attributable to surplus inventory working its way through the channel, rather than solely reflecting fresh expansion in end-market applications.

The research further points to added impetus from government-led initiatives in specific countries, most notably Spain and China. This nuance is significant because the appetite for cellular IoT modules is frequently propelled just as much by regulatory mandates or public-sector programs as it is by natural enterprise-driven digital transformation. Smart meter installations, payment terminals, utility networks, public infrastructure projects, and compliance-driven equipment replacement cycles can all generate concentrated surges in demand for particular module types, even when wider enterprise IoT investment stays restrained.

Berg Insight projects that cellular IoT module shipments will continue expanding at a compound annual growth rate of 7 percent until 2030, ultimately reaching 878 million units. Relative to the 33 percent spike observed in 2025, this forecast suggests that growth will settle back to a more moderate pace once the aftereffects of the inventory correction have faded.

Why this goes beyond a straightforward growth story

What sets this market assessment apart is the coexistence of strengthening demand with a fresh cost-related squeeze originating from outside the traditional IoT landscape. Berg Insight points out that the upward momentum has carried into 2026, but that memory chip pricing has emerged as a growing concern as memory producers redirect a larger share of their fabrication capacity toward high-bandwidth memory tailored for AI-centric servers and data center infrastructure.

This produces an uncommon cross-industry competitive pressure. Cellular IoT modules don’t directly rival AI servers in terms of their end-use applications, yet they are indirectly affected through overlapping semiconductor supply networks. The report suggests that the primary consequence so far has been upward pressure on component costs rather than actual supply shortages, with 5G modules bearing the brunt because they typically integrate a greater volume of memory and depend on more sophisticated DRAM architectures. Older-generation 4G LTE modules, which rely on more established memory technologies, face comparatively less disruption, though Berg Insight cautions that very few product lines remain entirely unaffected.

The practical takeaway is straightforward: module pricing is becoming more fluid. Suppliers are rolling out regular price reassessments and embedding contract-level provisions to absorb fluctuations in component expenses. For OEMs and systems integration firms, this can make long-horizon product roadmapping more challenging — particularly when the financial viability of a device hinges on predictable bill-of-materials costs stretched across multi-year deployment windows.

The vendor landscape remains tightly consolidated

The competitive configuration of the module market continues to be dominated by a handful of players. According to Berg Insight, Quectel, Fibocom, Telit Cinterion, MeiG, and China Mobile IoT collectively captured 73 percent of all cellular IoT module revenue in 2025.

Dominance in shipment volume, on the other hand, is heavily influenced by conditions within China’s home market. Quectel, China Mobile IoT, Sunsea AIoT, Lierda, and Fibocom are acknowledged as the top vendors by unit count, riding the wave of massive local procurement activity. Berg Insight also spotlights the fast-rising presence of ZXInfoTek, especially within the POS terminal vertical, a niche in which connectivity modules are closely bound to the rollout rhythms and refresh schedules of payment devices.

The chipset segment mirrors this same geographic pattern. Berg Insight calculates that shipments of cellular IoT chipsets — excluding automotive-qualified variants — amounted to 706 million units in 2025. ASR Microelectronics, Qualcomm, Eigencomm, UNISOC, Xinyi, and MediaTek served as the principal vendors. Chipset suppliers headquartered in China experienced a standout year in volume shipments, with ASR, Eigencomm, and Xinyi all posting meaningful gains in LTE Cat-1 bis and NB-IoT segments. Qualcomm maintained a strong foothold in LTE-M, premium 4G LTE, and 5G eMBB chipset offerings.

For connectivity service providers and large enterprises navigating this space, the report paints a picture of an increasingly fragmented planning landscape. Budget-friendly cellular IoT segments continue to gain scale, 5G module profitability remains more vulnerable to memory pricing dynamics, and selecting the right vendor now hinges more than ever on the intended application, regional market, and technological tier involved. The sector is once again on an upward trajectory, but the forces shaping its profitability are growing more intricate by the quarter.