")

Key Insights

- USD.AI is an onchain credit score structuring and funding protocol that funds GPU-backed, stablecoin-denominated loans for real-world AI infrastructure. Collateral is represented by the CALIBER framework, linking onchain representations to offchain authorized claims.

- The protocol makes use of a dual-token construction. USDai is designed for liquidity-sensitive capital, whereas sUSDai is yield-bearing and backed by longer-dated AI infrastructure loans. Redemption dynamics are managed by a queue-based mechanism.

- Our valuation mannequin treats execution because the binding constraint by separating pipeline originations from funded originations utilizing an specific funding realization fee to mirror {hardware} supply, set up, and settlement latency.

- CHIP is the governance and risk-policy token. It governs protocol parameters, treasury and capital coverage, and insurance coverage design. CHIP presently doesn’t have a mechanically enforced declare on protocol money flows, so worth accrual is modeled as contingent.

- Valuation is anchored by two lenses. (1) A buyback-supported pathway (reflecting governance-directed surplus routing) and (2) an insurance-capital-implied solvency threshold (reflecting capital adequacy constraint). Outputs suggest buyback-supported FDVs of $46.4M / $329.6M / $1.74B (bear/base/bull) and insurance-implied solvency thresholds of $270.1M / $275.6M / $503.2M.

Valuation Mannequin: The complete valuation mannequin, together with assumptions and state of affairs sensitivities, is accessible right here.

Introduction

USD.AI is an onchain credit score protocol financing real-world AI infrastructure. The protocol originates stablecoin-denominated loans backed by GPU {hardware} and associated compute belongings, bridging onchain capital with offchain infrastructure deployment.

The protocol points two core tokens, USDai, a dollar-denominated token used for minting, funding, and redemption flows, and sUSDai, a yield-bearing vault share representing publicity to deployed AI infrastructure loans. This construction separates liquid balances from capital that’s dedicated to longer-term loans. USDai doesn’t immediately take in loan-level credit score threat, whereas sUSDai holders explicitly bear amortization, redemption, and liquidity constraints in change for yield. This separation is central to USD.AI’s try and align onchain liquidity with real-world, longer-dated credit score belongings.

USD.AI’s structure combines DeFi primitives with authorized and operational frameworks tailor-made to real-world belongings. CALIBER offers the authorized and technical spine for representing GPU {hardware} as enforceable onchain collateral. Queue Extractable Worth (QEV) is the queue-based redemption mechanism used to handle liquidity in opposition to amortizing, illiquid collateral.

CHIP is the governance and utility token of the USD.AI DAO. It grants governance authority over protocol parameters, rate of interest controls, charge surfaces and charge routing, treasury and capital coverage, and the design of the staking and insurance coverage framework. Whereas protocol charges could also be directed towards buybacks or staking rewards sooner or later, there’s not presently a compulsory or mechanically enforced declare on protocol money flows.

The sections that observe consider USD.AI as a credit score infrastructure protocol and CHIP as a governance and threat coverage asset whose worth will depend on funded origination throughput, capital effectivity, and execution credibility somewhat than on assumed money circulate rights.

Understanding USD.AI

USD.AI sits between debtors looking for upfront capital to deploy AI compute infrastructure and capital suppliers looking for dollar-denominated yield. The protocol constructions collateral, underwrites threat, coordinates funding, and manages liquidity and redemption mechanics inside an onchain framework.

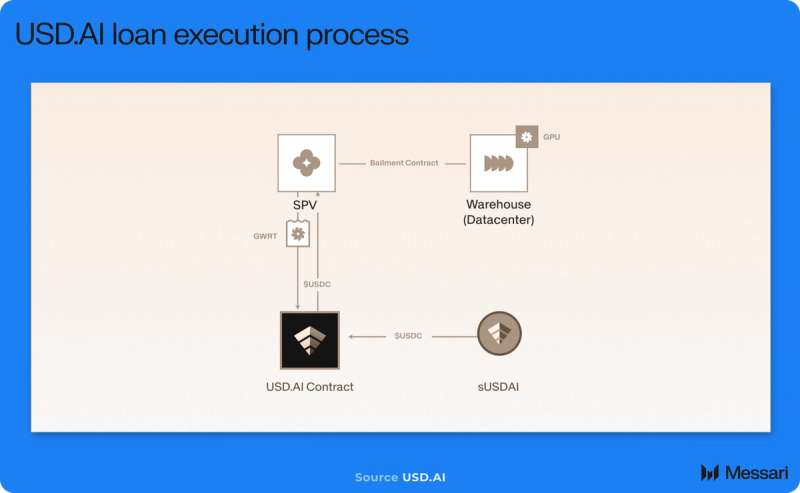

A central element of the structure is CALIBER, the technical framework used to characterize GPU {hardware} as enforceable collateral by linking onchain representations to offchain authorized claims. The intent is to make bodily compute belongings eligible for pooled, standardized credit score somewhat than structuring every mortgage as a bespoke personal association.

As soon as collateral is verified and accepted, USD.AI originates stablecoin-denominated loans backed by that {hardware}. Borrower onboarding, underwriting, and authorized structuring happen offchain, whereas mortgage balances, repayments, and associated financial flows are recorded and managed onchain.

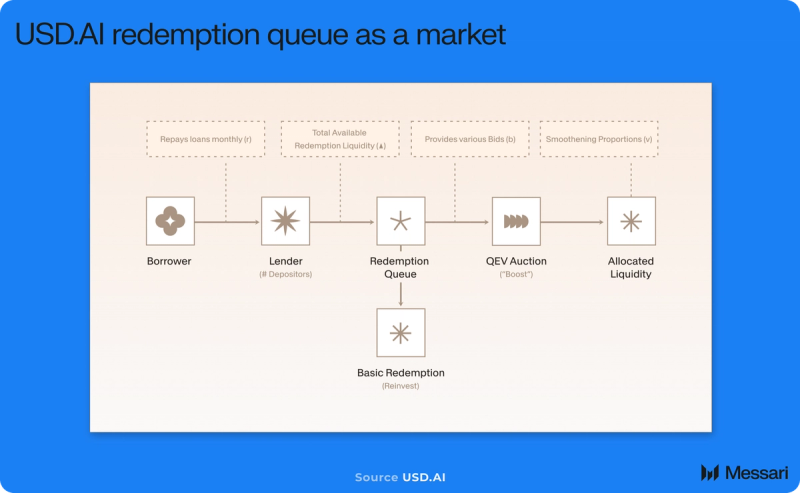

Infrastructure-backed lending inherently creates a structural liquidity mismatch. Underlying loans amortize over multi-year time horizons, whereas capital suppliers might search redemption sooner. USD.AI addresses this by queue-based redemptions for sUSDai. When liquidity is constrained, Queue Extractable Worth (QEV) costs redemption precedence inside the queue somewhat than counting on pressured asset gross sales or mounted liquidity buffers.

Underneath this design, redemptions are processed sequentially somewhat than instantaneously. If demand exceeds instantly out there liquidity, contributors might pay for precedence, permitting time desire to be expressed by market pricing. Liquidity constraints are made specific on the protocol stage and aligned with the amortizing profile of the underlying mortgage e-book.

USD.AI’s threat structure incorporates third-party collateral worth safety by Barker, an institutional valuation and risk-transfer platform. For GPU-backed loans originated by the protocol, Barker offers impartial collateral valuations and points a contractual guarantee on these valuations. The guarantee is absolutely reinsured by Munich Re by its aiSure efficiency assure.

Protection is structured at 80% of Barker’s independently assessed collateral valuation. As a result of USD.AI caps loans at a most 80% loan-to-value (LTV) ratio, the construction is designed to offer protection equal to the total excellent principal quantity at origination beneath normal underwriting assumptions.

If liquidation proceeds fall under the lined valuation threshold, the shortfall is contractually payable to the protocol, topic to the governing coverage phrases, circumstances, and exclusions. For instance, if collateral is valued at $10.0 million and a mortgage is originated at $8.0 million (80% LTV), protection is about at $8.0 million. If liquidation yields $7.2 million web, the insured construction is designed to cowl the $0.8 million distinction, bringing complete restoration to the lined threshold.

The premium for this protection is paid by the protocol and embedded in mortgage economics, lowering web yield out there to sUSDai holders. Relative to the prior FiLo tranche construction, the insurance-backed mannequin is designed to be materially extra capital-efficient. Protection prices decline from the junior tranche mannequin to the Barker guarantee construction, whereas eliminating the necessity to fund and compensate a devoted first-loss tranche.

This shift reduces structural capital depth and redirects economics that will beforehand have accrued to junior tranche holders again towards sUSDai. Whereas the construction materially mitigates principal loss severity beneath outlined circumstances, it doesn’t get rid of valuation mannequin threat, claims-processing threat, liquidity timing threat, contractual exclusions, or excessive market dislocation threat.

CHIP Tokenomics

CHIP is the governance and utility token of the USD.AI protocol. It governs protocol requirements, threat parameters, charge surfaces and charge routing, rate of interest controls, and capital coverage. Whereas protocol charges could also be directed towards buybacks or staking rewards, there’s presently not a compulsory or mechanically enforced declare on protocol money flows.

CHIP’s utility might be grouped into three major domains:

- Governance and protocol management

CHIP holders govern the USD.AI DAO and set high-level parameters that form credit score formation and system threat. These embrace collateral eligibility requirements, underwriting thresholds, rate of interest controls, liquidity and redemption settings, insurance coverage protection necessities, and treasury coverage. By means of these levers, governance determines how the protocol balances origination development, capital effectivity, and systemic resilience. - Income governance and capital allocation

CHIP governs the protocol’s charge surfaces, together with origination and servicing charges, web curiosity margin, administrative charges, and liquidity-related charges. Governance additionally determines how collected charges are routed, together with potential allocations to working bills, reinvestment, staking incentives, or token buybacks. As a result of charge routing is ruled somewhat than hard-coded, surplus seize by tokenholders is policy-dependent somewhat than computerized. - Staking module and threat backstop

CHIP might be staked right into a protocol-defined staking module designed to help system security and alignment. Stakers obtain rewards sourced from protocol charges or designated incentives and settle for predefined lock and slashing circumstances tied to goal shortfall occasions. To the extent that staked CHIP is acknowledged as backstop capital inside the insurance coverage framework, token worth turns into partially linked to protection necessities, staking participation, and collateral recognition parameters.

CHIP disclosed tokenomics are as follows:

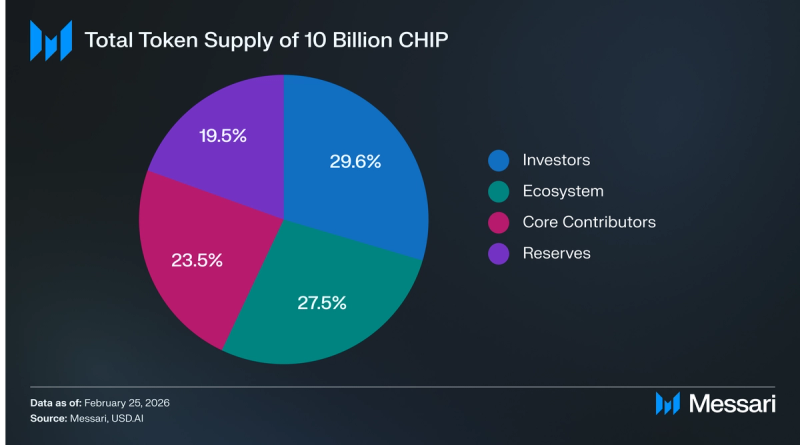

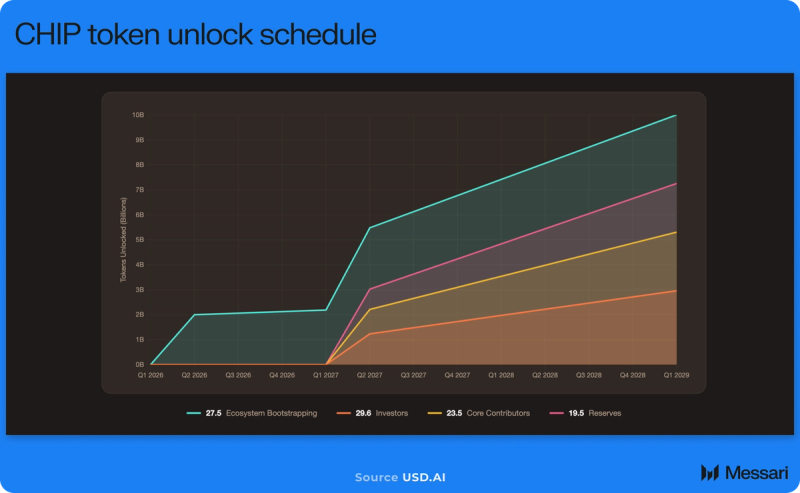

- Whole token provide: 10,000,000,000

- Allocation breakdown: 29.6% traders, 27.5% ecosystem bootstrapping, 23.5% core contributors, and 19.5% reserves.

- Vesting schedules and lockups: Investor and core contributor allocations observe the identical schedule – 0% unlocked earlier than month 12, 33% unlocked at month 12, and the remaining 67% unlocked in equal month-to-month installments over the next 24 months. Ecosystem and reserve allocations are topic to governance-directed deployment.

Valuation Framework

CHIP doesn’t have an computerized declare on protocol money flows. Governance controls charge routing and capital coverage, however surplus allocation to tokenholders is discretionary somewhat than mechanically enforced.

Accordingly, we don’t apply a conventional equity-style discounted money circulate that assumes sturdy and enforceable surplus routing. As a substitute, our valuation begins with observable protocol economics, resembling pipeline originations, charge era, and value construction, after which explicitly fashions the circumstances beneath which these economics might translate into tokenholder worth.

We mannequin CHIP utilizing two complementary lenses:

- Buyback-supported worth

CHIP is modeled as a governance asset which will seize surplus by discretionary buybacks. Buybacks are contingent on a DAO-enabled routing resolution and are subsequently modeled as a scenario-based coverage variable somewhat than a assured entitlement. - Insurance coverage-capital-implied solvency threshold

CHIP is modeled as backstop capital inside the insurance coverage module. This lens estimates the absolutely diluted valuation required for staked and acknowledged CHIP to fulfill said protection necessities beneath specific assumptions about publicity, protection ratios, staking participation, collateral recognition, and required staking yield. The output represents a solvency-consistent capitalization stage, not a worth goal.

Collectively, these lenses create a coherent bridge from protocol exercise to token worth with out imposing enforceable money circulate rights the place none are encoded.

USD.AI’s major execution threat is changing the pipeline into funded originations. The mannequin subsequently distinguishes between:

- Pipeline mortgage originations: gross sales and underwriting throughput.

- Funding realization fee: the latency-adjusted conversion fee from pipeline to funded quantity.

- Funded originations: the economically related quantity that drives charge income and fee-funded incentives.

This separation prevents the pipeline from being handled as income and concentrates state of affairs differentiation on execution somewhat than demand.

Protocol income is modeled by discrete elements somewhat than a blended take fee:

- Origination charge income: modeled as funded originations multiplied by an origination charge fee.

- Service charge income: included as an specific line merchandise however conservatively disabled within the base case as a consequence of undisclosed charge charges.

- QEV-related charges: modeled as a operate of redemption quantity and a QEV charge fee, reflecting that QEV is an specific liquidity primitive supposed to handle redemption flows.

- Liquidation charges: modeled as a tail-event income stream and disabled within the base case, given restricted disclosure round realized default pathways and liquidation frequency.

This method is deliberately conservative. It avoids inventing income sources whereas preserving a whole framework that may be up to date because the protocol publishes charge schedules and realized charge mixes.

As a result of USD.AI is positioned as a credit score structuring and funding protocol somewhat than a everlasting balance-sheet lender, we don’t apply a bank-style anticipated credit score loss framework. As a substitute, the mannequin assumes that the protocol earns web curiosity on excellent publicity through the interval loans are funded and held, web of depositor yield and required liquidity buffers. Residual threat is captured by an specific friction adjustment somewhat than by lifetime anticipated credit score losses.

The mannequin, subsequently, contains:

- Collateral worth safety premiums, modeled as a price on the typical mortgage e-book. This represents the protocol-paid premium for third-party collateral worth warranties offered by the Barker framework and reinsured by Munich Re. The premium reduces web curiosity earnings and immediately impacts the yield out there to sUSDai holders.

- Working prices, anchored to a largely mounted baseline with modest scaling, reflecting administration steering that OpEx is comparatively predictable over the forecast horizon.

Working surplus is outlined as web protocol income much less working prices and safety premiums. Distributable surplus displays the portion out there after required reserves and system help prices.

As a result of surplus routing is governance-contingent, buybacks are modeled explicitly by:

- Buyback fee: the share of distributable surplus routed to buybacks.

- Buyback effectiveness: a buyback effectivity issue capturing execution high quality and market influence, which prevents overstating how effectively {dollars} translate into token help.

Terminal worth is estimated by making use of a a number of to 12 months 5 distributable surplus and discounting at scenario-specific charges. This capabilities as a market-pricing lens somewhat than an enforceable DCF.

Individually, we estimate an insurance-capital-implied solvency threshold to mirror CHIP’s potential function as acknowledged backstop capital inside the protocol’s insurance coverage framework. Underneath this lens, required backstop capital scales with the modeled excellent funded publicity and an assumed insurance coverage protection ratio. That requirement is then adjusted for the share of tokens actively staked and for the proportion of staked tokens acknowledged as usable insurance coverage capital. Lastly, we incorporate a required staking yield to mirror the return demanded by capital suppliers for bearing tail threat.

The ensuing threshold represents the absolutely diluted valuation at which staked and acknowledged CHIP can be adequate to satisfy the protocol’s protection requirement beneath modeled assumptions. Enhancements in capital effectivity can cut back this threshold at the same time as working efficiency strengthens.

The state of affairs set is designed to bracket believable outcomes by concentrating uncertainty within the handful of variables that matter:

- Pipeline scale: how rapidly annual originations broaden.

- Funding realization: the latency and conversion fee from pipeline to funded quantity.

- Price charges and charge combine: primarily origination charges, with non-compulsory service and QEV charges gated till disclosed.

- Capital coverage: buyback fee and buyback effectiveness, explicitly handled as governance-contingent.

- Insurance coverage parameters: protection requirement, collateral recognition charges, and required staking yield.

The valuation framework might be summarized as:

Pipeline originations → funding realization → funded originations → charge income → safety value and working prices → distributable surplus → governance-contingent buybacks

In parallel, the solvency lens follows a capital adequacy path:

Excellent funded publicity → protection requirement → acknowledged backstop capital → staking participation and recognition fee → required staking return → insurance-capital-implied solvency threshold

This construction preserves rigor beneath uncertainty. It avoids imposing money circulate rights that aren’t mechanically encoded but, whereas nonetheless capturing the 2 credible pathways by which CHIP may accrue worth if the protocol implements the mechanisms it has indicated publicly.

It’s possible you’ll view our full valuation mannequin right here.

Whole Addressable Market

USD.AI’s near-term complete addressable market (TAM) shouldn’t be “global AI spend” within the summary. The economically related TAM for CHIP is the subset of worldwide GPU CapEx that’s (1) financeable, (2) addressable by USD.AI’s collateral and underwriting stack (CALIBER), and (3) fundable onchain beneath the protocol’s liquidity design (QEV).

USD.AI is positioning itself as a credit score origination and funding for real-world AI infrastructure, not as a generalized AI or stablecoin protocol. Consequently, the binding constraint on scale shouldn’t be the theoretical demand for AI compute, however the portion of GPU deployments that may be structured into enforceable, tokenized collateral and reliably funded by onchain capital markets.

This boundary is about by collateral enforceability and liquidity design, which decide what share of GPU CapEx might be financed onchain at scale.

World GPU CapEx Assumptions

There is no such thing as a single reported determine for international GPU CapEx. To assemble a defensible baseline, we start with broader information heart capital expenditure and isolate the portion attributable to AI accelerators and GPU-based methods. Nonetheless, trade analysis offers directional anchors. Omdia initiatives international information heart CapEx reaching roughly $1.6 trillion yearly by 2030, whereas McKinsey estimates cumulative information heart funding of roughly $6.7 trillion by the top of the last decade. Present hyperscaler disclosures and vendor income trajectories suggest that present-day international information heart CapEx is already within the a number of hundred-billion-dollar vary.

Inside that complete, accelerator-driven funding is quickly rising. Trade evaluation from corporations resembling Dell’Oro signifies AI chips and accelerator methods account for roughly one-third of information heart CapEx and are growing as AI workloads broaden.

Utilizing these anchors, we estimate the present annual AI accelerator and GPU system CapEx at roughly $200-250 billion. This determine excludes non-financeable elements, resembling land, buildings, and energy infrastructure, and focuses as a substitute on {hardware} methods that would plausibly function collateral for structured credit score. We anchor 12 months 1 of the mannequin at $250 billion, the higher finish of that vary.

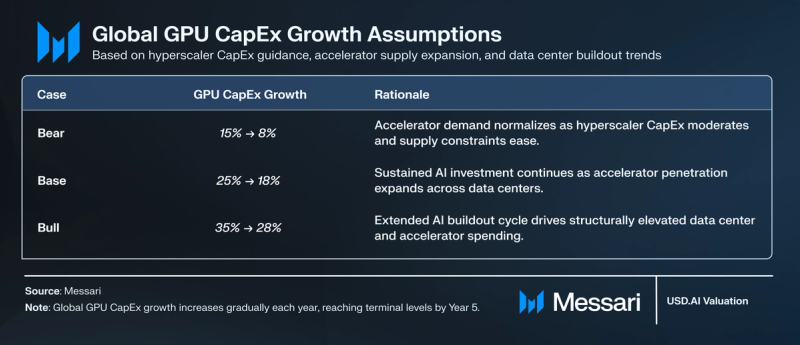

Development assumptions mirror continued AI infrastructure scaling implied by hyperscaler funding plans and accelerator provide enlargement:

- Bear case: 15% (12 months 1) → 8% (12 months 5)

Assumes AI infrastructure development decelerates meaningfully as provide constraints ease and hyperscaler CapEx normalizes. GPU system spending continues to broaden however transitions towards a extra mature mid-cycle development profile by 12 months 5. - Base case: 25% (12 months 1) → 18% (12 months 5)

Displays sustained however moderating enlargement according to hyperscaler disclosures and vendor backlog commentary. Development slows because the put in base will increase, however accelerator penetration in information facilities continues to rise. Underneath this trajectory, annual AI accelerator CapEx approaches roughly $600 billion by 12 months 5. - Bull case: 35% (12 months 1) → 28% (12 months 5)

Represents an prolonged infrastructure buildout cycle through which AI workloads drive continued acceleration in information heart funding. Development stays structurally elevated by the forecast interval, supported by enterprise adoption and sustained accelerator provide enlargement.

Underneath the bottom trajectory, annual AI accelerator CapEx approaches roughly $600 billion by 12 months 5, according to projected information heart enlargement and the rising accelerator share of complete infrastructure funding.

Financeable share of GPU CapEx

Not all GPU CapEx is realistically financeable by structured credit score. The mannequin subsequently applies a financeable share to international AI accelerator spending to mirror structural constraints, together with:

- hyperscaler self-funding and vertical integration,

- strategic deployments financed immediately off company steadiness sheets,

- jurisdictional, authorized, or custody limitations,

- and asset traits that restrict collateral enforceability.

We assume financeable shares starting from 15% within the bear case, 25% within the base case, and 35% within the bull case.

This vary is knowledgeable by broader infrastructure finance observe. In conventional infrastructure sectors, initiatives that use exterior financing typically make use of significant leverage, with debt representing a considerable share of complete capital construction. Nonetheless, infrastructure debt fundraising represents solely a subset of total infrastructure capital formation, reflecting that many belongings are funded immediately by company steadiness sheets or giant sponsors somewhat than by formal mission or structured debt automobiles.

Structured credit score penetration, subsequently, varies by asset class, sponsor energy, and market cycle. In early AI infrastructure buildouts, hyperscalers and well-capitalized expertise corporations usually tend to self-fund {hardware} funding, lowering third-party debt participation relative to mature infrastructure segments. Over time, impartial operators, co-location suppliers, and mid-market services might more and more depend on asset-backed financing as collateral frameworks mature.

Underneath this logic:

- Bear case (15%) assumes continued focus amongst self-funded hyperscalers and restricted structured credit score penetration.

- Base case (25%) displays reasonable participation by third-party credit score suppliers according to noticed infrastructure debt market participation.

- Bull case (35%) assumes broader adoption of asset-backed constructions as collateral enforceability improves and financing markets deepen.

This parameter capabilities as a macro financing filter somewhat than a protocol adoption variable. It converts complete accelerator funding into the portion realistically addressable by third-party credit score suppliers. USD.AI’s market share assumptions are then utilized to this financeable base, somewhat than to complete GPU CapEx.

Adoption and Origination Quantity

USD.AI’s financial mannequin is origination-driven. Price income is generated at origination, whereas excellent publicity determines liquidity necessities, collateral safety prices, and capital allocation capability. Because of this, adoption is modeled by origination throughput somewhat than notional TVL or passive steadiness development.

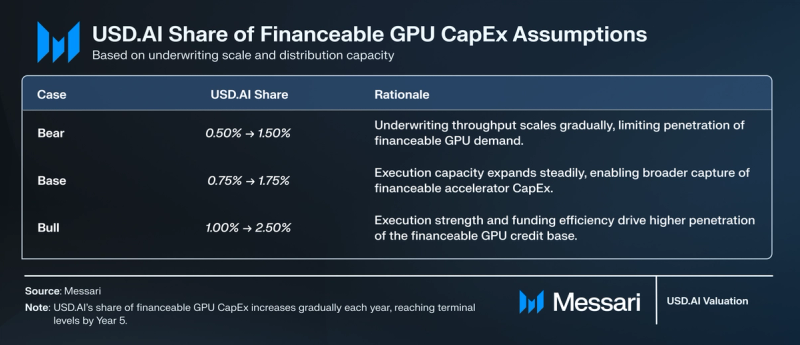

USD.AI share of financeable CapEx

We mannequin USD.AI’s adoption as a share of financeable GPU CapEx, with a five-year penetration ramp that varies by state of affairs. This share captures underwriting capability, borrower acquisition, distribution attain, and aggressive positioning in GPU infrastructure finance.

We assume the next penetration path of financeable CapEx:

- Bear: 0.50% (12 months 1) → 1.50% (12 months 5)

- Base: 0.75% (12 months 1) → 1.75% (12 months 5)

- Bull: 1.00% (12 months 1) → 2.50% (12 months 5)

The bear case assumes underwriting throughput scales slowly, limiting penetration of the addressable financing base. The bottom case displays regular execution enchancment and gradual enlargement of distribution capability. The bull case assumes each sturdy funding realization and materially greater market share seize as USD.AI scales underwriting capability, borrower acquisition, and capital formation in parallel.

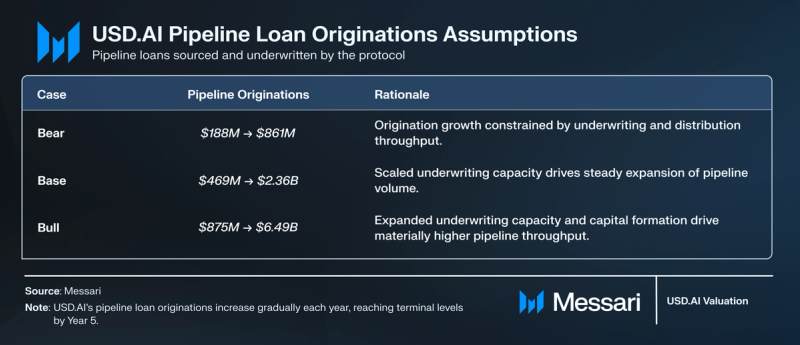

Making use of these shares to the financeable CapEx base produces the next pipeline mortgage originations:

- Bear: $188M (12 months 1) → $861M (12 months 5)

- Base: $469M (12 months 1) → $2.36B (12 months 5)

- Bull: $875M (12 months 1) → $6.49B (12 months 5)

These figures characterize pipeline originations, outlined as loans sourced, underwritten, and marketed by the protocol. They mirror underwriting and distribution throughput somewhat than funded quantity.

Upcoming loans complete roughly $105.7 million in principal, anchoring the near-term pipeline in opposition to which the modeled origination ramps ought to be evaluated. Funding realization is modeled individually to transform pipeline into economically energetic publicity.

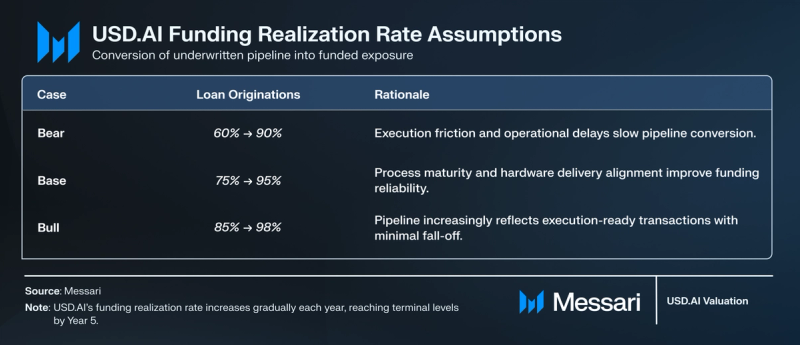

Mortgage latency and funding realization

The mannequin separates pipeline originations from funded originations by an specific funding realization fee. This parameter captures execution constraints resembling {hardware} supply timelines, set up schedules, authorized settlement, and collateral perfection.

We assume the next funding realization paths:

- Bear: 60% (12 months 1) → 90% (12 months 5)

- Base: 75% (12 months 1) → 95% (12 months 5)

- Bull: 85% (12 months 1) → 98% (12 months 5)

The modeled realization charges assume pipeline displays credit-vetted, operationally advancing transactions somewhat than early-stage advertising leads. In personal credit score and infrastructure finance, conversion varies considerably by stage: late-stage, mandated offers sometimes shut at excessive charges, whereas early-stage pipeline reveals larger fall-off. The bear case displays sustained execution friction, whereas the bottom and bull instances assume pipeline more and more represents execution-ready transactions as processes mature.

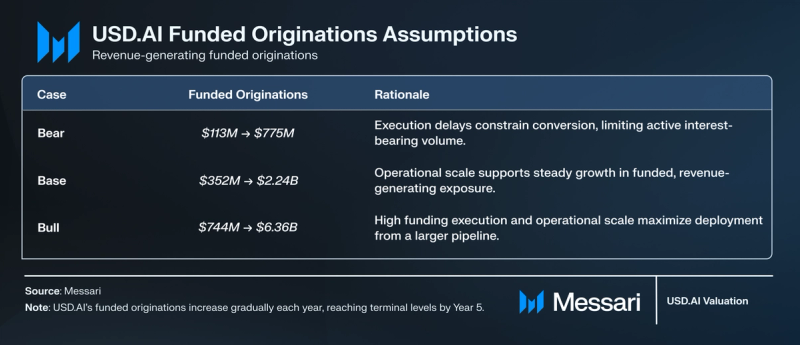

Making use of these realization charges to pipeline originations yields the next funded volumes:

- Bear: $113M (12 months 1) → $775M (12 months 5)

- Base: $352M (12 months 1) → $2.24B (12 months 5)

- Bull: $744M (12 months 1) → $6.36B (12 months 5)

Funded originations characterize economically energetic quantity. Price era, web curiosity earnings, liquidity necessities, and collateral safety sizing are all pushed by funded publicity somewhat than the marketed pipeline. This separation prevents pipeline from being handled as revenue-bearing and concentrates valuation sensitivity on operational execution somewhat than headline demand.

Protocol Income Mannequin

Protocol income is modeled by specific financial elements somewhat than a blended take fee. This method ensures consistency between origination quantity, excellent publicity, liquidity buffers, funding prices, and charge streams, and prevents double-counting between unfold earnings and specific charges.

Web curiosity earnings and funding prices

Web curiosity earnings (NII) is modeled as the mix of three elements:

- Curiosity earnings on funded loans, calculated by making use of borrower APR assumptions to common excellent publicity.

- Curiosity earnings on liquidity reserves, representing yield earned on unutilized capital held to help redemptions and operational liquidity.

- Depositor yield expense, utilized to the sUSDai-funded portion of common TVL and modeled as a time-varying collection somewhat than a set fixed.

Within the base case, borrower APR is assumed at 15%, defining the gross yield on funded publicity. Idle liquidity is assumed to earn roughly 3.6%, according to short-duration T-bill equivalents. Depositor yield on sUSDai begins round 9.0% and step by step rises to 10.8% over the forecast horizon, reflecting aggressive funding circumstances and protocol maturity.

A 0.50% collateral safety premium is utilized to the typical mortgage e-book to mirror third-party valuation guarantee prices beneath the Barker construction. The mannequin additionally assumes a goal utilization ramp and specific liquidity buffers, which go away a portion of capital briefly undeployed at any given time. As a result of not all capital is repeatedly incomes borrower APR, this unused steadiness reduces efficient web curiosity earnings relative to full deployment.

Web curiosity unfold is subsequently pushed by borrower pricing, capital deployment effectivity, required liquidity buffers, and depositor yield dynamics.

Public liquidity incentives, together with the PYUSD incentive program (4.5% on eligible deposits), can affect depositor economics. The mannequin doesn’t deal with such packages as structural income or everlasting unfold enhancement. As a substitute, any impact is mirrored by depositor yield assumptions and capital allocation into sUSDai. Within the base case, web curiosity earnings displays borrower pricing, liquidity buffers, and depositor yield expense with out assuming ongoing exterior subsidy.

Price income

Along with spread-based earnings, the mannequin contains 4 distinct charge streams, every tied to an outlined protocol mechanism. Even the place sure charges are set to zero within the base case, they’re modeled individually somewhat than embedded in a blended take fee.

- Origination charges, utilized to pipeline mortgage originations and differ by state of affairs. That is the first disclosed charge stream and the dominant driver of non-spread income.

- Service charges, utilized to the typical excellent mortgage e-book. These are parameterized however set to zero within the base case pending clearer disclosure of the charge base and fee.

- QEV-related charges, modeled as a operate of common TVL, an assumed redemption fee, and a QEV charge parameter. These are conservatively sized, reflecting QEV’s said function as a liquidity coordination mechanism somewhat than a core income engine.

- Liquidation charges, utilized to funded originations. These are set to zero within the base case, given restricted public disclosure of realized default frequency and fee-capture mechanics.

Modeling these elements individually maintains inside consistency between origination circulate, publicity, liquidity dynamics, and charge seize. As charge schedules and realized economics develop into clearer, particular person traces might be adjusted with out altering the broader income framework.

Residual threat and friction losses

Third-party collateral worth safety materially reduces loss severity however doesn’t suggest zero financial leakage. Even in an insured construction, realized outcomes can diverge from modeled recoveries as a consequence of valuation foundation threat, coverage phrases and exclusions, claims processing timelines, liquidation prices, and operational frictions.

To mirror this, the mannequin applies a residual friction adjustment to funded publicity. This haircut represents a share discount supposed to seize financial leakage which will persist even when principal publicity is contractually protected.

The adjustment incorporates potential settlement inefficiencies, divergence between insured valuation benchmarks and realized liquidation proceeds, claims timing delays, contractual exclusions, and edge-case enforcement disputes. Though GPU collateral is roofed by third-party worth safety, real-world credit score methods not often obtain excellent restoration. The friction adjustment ensures the mannequin doesn’t overstate web economics whereas avoiding a full anticipated credit score loss framework that will be inconsistent with USD.AI’s insured construction.

Working Bills

Working bills are modeled as a mix of mounted overhead and scale-linked servicing prices:

Working Prices = $5 million mounted base + 0.25% × Ending Excellent Mortgage E-book

The $5 million mounted element in 12 months 1 is according to administration steering relating to the steady-state value base required to help underwriting, authorized structuring, insurance coverage coordination, and protocol operations. This displays a lean however institutionally credible working footprint somewhat than a completely scaled monetary platform.

Bills scale with funded mortgage e-book development somewhat than income. As excellent publicity will increase, incremental prices come up from credit score monitoring, collateral oversight, reporting infrastructure, and compliance necessities. This construction aligns the mannequin with specialty finance platforms, the place working depth expands with belongings beneath administration somewhat than with top-line development.

Working Surplus and Capital Allocation Boundary

Working surplus is outlined as web protocol income after working bills and residual threat changes. It represents pre-allocation earnings generated by the protocol.

Nonetheless, working surplus shouldn’t be robotically distributable. USD.AI requires ongoing capital to help liquidity buffers, collateral safety prices, and system resilience. The mannequin, subsequently, introduces an specific boundary between working efficiency and the worth out there for discretionary use.

Distributable surplus is outlined as working surplus web of required reserves and system help prices. That is the portion of earnings that governance may allocate towards buybacks, staking incentives, treasury technique, or reinvestment.

Separating working surplus from distributable surplus prevents the implicit assumption that every one protocol earnings accrue to CHIP holders. In a system the place liquidity administration and capital adequacy are core design options, retained earnings could also be structurally essential.

This distinction is central to the valuation framework. It ensures that:

- Worth accrual to CHIP is contingent on governance, not mechanically assumed.

- Capital coverage is constrained by system security necessities.

- Surplus routing might be stress-tested independently from working efficiency.

This capital boundary underpins the 2 lenses utilized to CHIP: an upside lens tied to governance-directed surplus allocation, and a capital adequacy constraint tied to CHIP’s potential function as acknowledged insurance coverage capital.

Token Worth Accrual for CHIP

Buyback-supported worth

The buyback-supported lens evaluates CHIP as a governance asset which will seize worth by discretionary surplus allocation. A portion of distributable surplus could also be directed towards token buybacks, topic to DAO coverage. This pathway is modeled explicitly as a governance selection somewhat than a contractual entitlement.

The framework proceeds as follows:

- Projected distributable surplus (Years 1-5) → discounted to current worth = PV of distributable surplus

- 12 months 5 distributable surplus × terminal enterprise a number of → terminal enterprise worth → discounted to current worth = PV of terminal enterprise worth

- PV of distributable surplus + PV of terminal enterprise worth = complete enterprise worth

- Whole enterprise worth × buyback fee × buyback effectiveness = buyback-supported CHIP worth

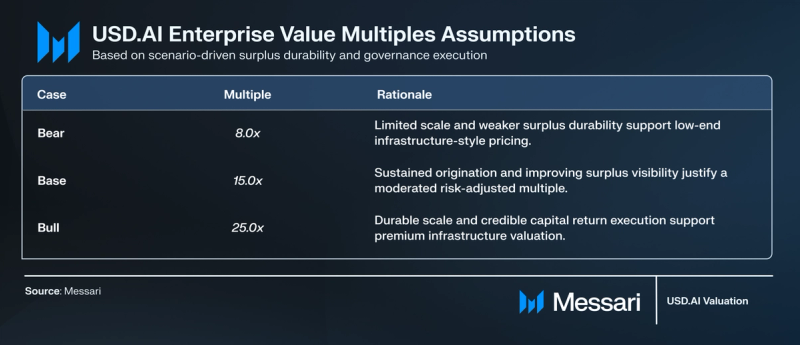

We estimate a terminal enterprise worth by making use of an EV a number of to 12 months 5 distributable surplus. This a number of is a market-pricing assumption reflecting how traders might worth a governance-directed surplus stream as soon as scale, sturdiness, and capital coverage credibility are observable.

Terminal multiples differ by state of affairs:

- Bear (8×): Assumes restricted scale and weaker confidence in sturdy surplus formation and capital return coverage, leading to infrastructure-like low-end pricing.

- Base (15×): Assumes sustained origination throughput and enhancing sturdiness, however with governance-contingent capital return nonetheless priced with a threat premium.

- Bull (25×): Assumes sturdy scale, improved predictability of distributable surplus, and credible, repeatable capital return execution, supporting a premium valuation according to scaled onchain credit score platforms.

Each distributable surplus (Years 1-5) and terminal enterprise worth are discounted to current worth utilizing scenario-specific low cost charges of 25% (bear), 20% (base), and 15% (bull). These charges incorporate execution threat, governance-contingent surplus routing, crypto market cyclicality, and structural uncertainty inherent in an early-stage onchain credit score platform. Increased charges in weaker eventualities mirror elevated uncertainty round origination scale, funding realization, and coverage sturdiness.

The buyback fee and buyback effectiveness govern how surplus interprets into token help. Within the core valuation, we assume a 50% buyback fee and 75% buyback effectiveness throughout instances. These parameters mirror partial surplus allocation and reasonable execution effectivity, and are diversified within the sensitivity evaluation.

Underneath these assumptions, the mannequin produces the next buyback-supported absolutely diluted valuations (FDV):

- Bear: $46.4M

- Base: $329.6M

- Bull: $1.74B

Variation throughout eventualities is pushed by variations in origination scale, funding realization, web curiosity economics, low cost charges, and terminal multiples utilized to distributable surplus. The evaluation avoids round worth assumptions and derives token worth strictly from modeled working efficiency and explicitly outlined capital coverage parameters.

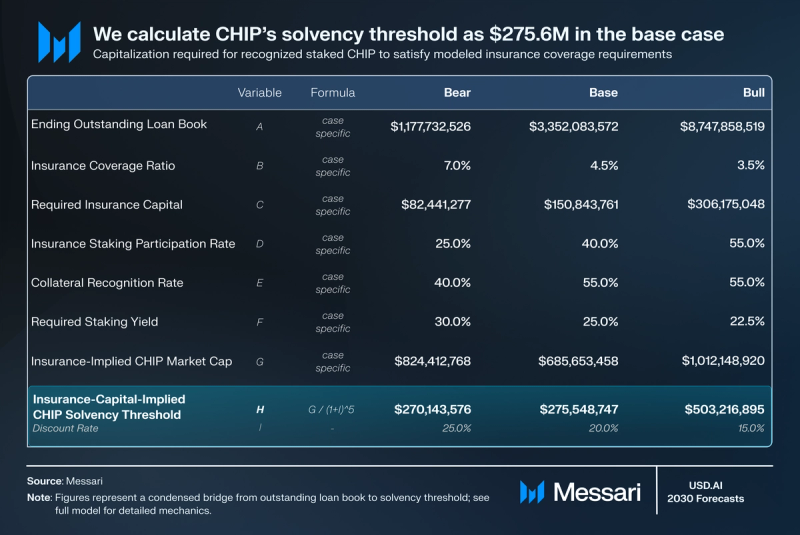

Insurance coverage-capital-implied solvency threshold

We additionally mannequin an insurance-capital-implied solvency threshold based mostly on CHIP’s potential function as acknowledged backstop capital inside the protocol’s insurance coverage module.

This lens evaluates the absolutely diluted valuation at which staked and acknowledged CHIP can be adequate to fulfill the protocol’s insurance coverage protection requirement beneath specific assumptions about publicity, protection ratios, staking participation, collateral recognition charges, and required staking yield.

The calculation begins with the modeled excellent funded publicity of the protocol. A protection ratio is utilized to that publicity to find out the quantity of required backstop capital. This capital requirement is then adjusted for staking participation, outlined as the proportion of complete token provide actively staked, and for the collateral recognition fee, outlined because the proportion of staked CHIP acknowledged as usable insurance coverage capital.

The solvency threshold is pushed by 4 core parameters, which differ by state of affairs:

- Insurance coverage protection ratio: 7.0% (bear), 4.5% (base), 3.5% (bull), representing required backstop capital as a share of excellent funded publicity.

- Staking participation: 25% (bear), 40% (base), 55% (bull), reflecting the portion of complete token provide actively staked.

- Collateral recognition fee: 40% (bear), 55% (base and bull), representing the proportion of staked CHIP acknowledged as usable insurance coverage capital for protection functions.

- Required staking yield: 30% (bear), 25% (base), 22.5% (bull), representing the return demanded by backstop capital suppliers given perceived protocol threat.

Insurance coverage protection ratio is the dominant mechanical driver of required capital. Staking participation and recognition fee decide how effectively token provide interprets into usable protection, whereas required staking yield determines the capitalization essential to compensate capital suppliers for threat. Increased required yields improve the implied threshold; decrease required yields compress it.

Underneath the mannequin assumptions, the ensuing discounted insurance-capital-implied solvency thresholds are:

- Bear: $270.1M

- Base: $275.6M

- Bull: $503.2M

This output shouldn’t be interpreted as a worth flooring or intrinsic valuation anchor. It displays the capitalization required to keep up protection on the modeled publicity stage. Increased protection necessities or decrease recognition charges improve required capitalization, whereas improved staking participation or recognition effectivity cut back the capital required per unit of publicity.

Accordingly, the implied solvency threshold can decline in stronger working eventualities if capital effectivity improves. Such declines mirror lowered capital depth somewhat than weaker working efficiency.

Reconciling the Two Analytical Lenses

The 2 analytical lenses utilized to CHIP are deliberately not collapsed right into a single level estimate as a result of they reply completely different financial questions.

The buyback-supported pathway displays discretionary upside participation in working efficiency, conditional on governance credibility and capital return execution. It turns into most informative when the DAO demonstrates sustained, repeatable surplus allocation.

The insurance-capital-implied solvency threshold displays the capitalization stage required for the system to fulfill its protection necessities if CHIP capabilities as acknowledged backstop capital. It doesn’t characterize intrinsic worth or a worth flooring. As a substitute, it defines the valuation according to capital adequacy beneath specified assumptions about publicity, staking participation, protection ratios, and collateral recognition.

Divergence between these outputs is predicted. The buyback pathway scales with distributable surplus and market pricing of sturdiness, whereas the solvency threshold scales with publicity and capital depth. Enhancements in capital effectivity can cut back the solvency threshold even because the surplus-driven valuation potential will increase.

Sensitivity Evaluation

CHIP’s outcomes are evaluated throughout three sensitivity tables, every similar to a definite financial layer of the framework: market pricing, governance execution, and capital adequacy.

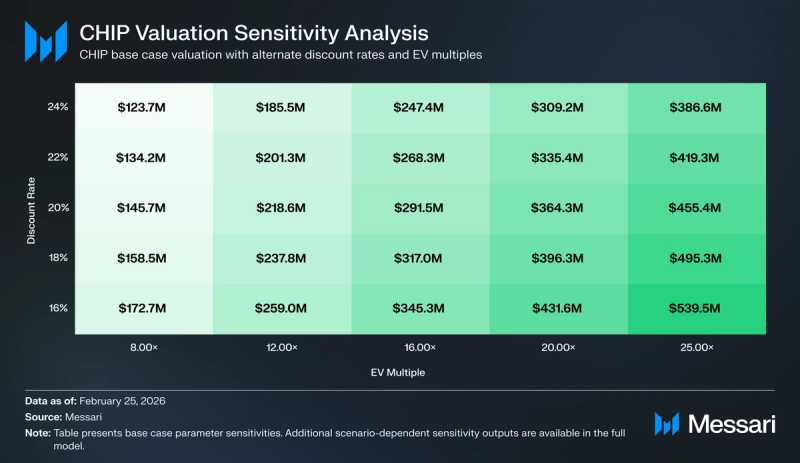

Buyback-supported worth: market-pricing sensitivity

The primary sensitivity desk evaluates the buyback-supported FDV throughout a grid of terminal EV multiples and low cost charges, holding protocol mechanics fixed. EV multiples vary from 8× to 25×, whereas low cost charges span 16% to 24%, reflecting a large however defensible band for discretionary, governance-contingent surplus.

In weaker eventualities, valuation dispersion throughout this grid is comparatively contained. At low origination scale and restricted distributable surplus, even aggressive multiples or decrease low cost charges produce solely incremental upside. This displays a easy constraint that when surplus is small in absolute phrases, modifications in valuation multiples or low cost charges have restricted influence.

Within the base state of affairs, sensitivity turns into extra balanced. Shifting from an 8× to a 16× a number of, or from a 24% to an 18% low cost fee, produces significant modifications in FDV, reflecting some extent at which surplus exists and valuation will depend on how traders worth sturdiness and governance credibility somewhat than on whether or not the system works in any respect.

In stronger eventualities, dispersion is pushed primarily by the terminal a number of somewhat than the low cost fee. At EV multiples between 16× and 25×, valuation outcomes broaden quickly, indicating that upside is more and more decided by market re-rating of USD.AI as a sturdy onchain credit score platform, somewhat than additional enhancements in origination throughput.

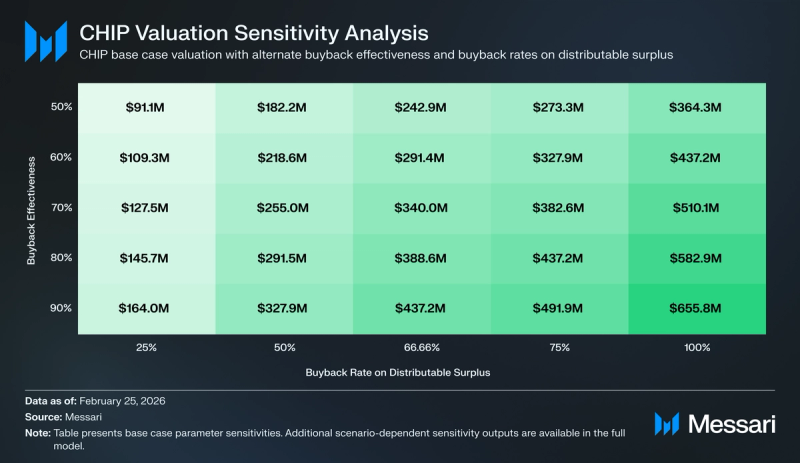

Buyback-supported worth: governance execution sensitivity

The second buyback sensitivity desk evaluates how distributable surplus interprets into token help, with two explicitly governance-contingent variables:

- Buyback fee, starting from 25% to 100% of distributable surplus.

- Buyback effectiveness, starting from 50% to 90%, represents the proportion of nominal buyback spend that interprets into sturdy token provide discount after accounting for liquidity depth and market influence.

This desk makes clear that buyback-supported worth shouldn’t be merely a operate of working efficiency. Even at equivalent surplus ranges, outcomes differ materially relying on whether or not governance prioritizes buybacks and whether or not these buybacks are executed effectively.

At low buyback charges or low effectiveness, a big portion of financial worth fails to translate into sustained buy-side stress. Conversely, excessive buyback charges mixed with sturdy effectiveness materially amplify token help. This sensitivity reinforces the mannequin’s core framing that buyback-supported worth is a coverage consequence, not an entitlement.

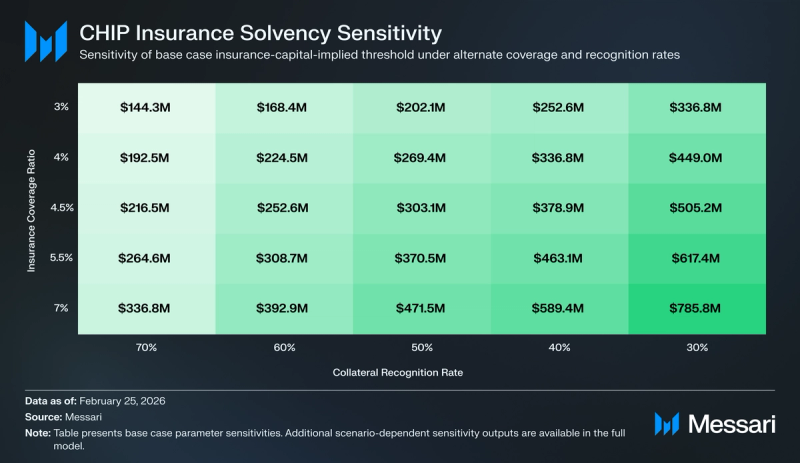

Insurance coverage-capital-implied solvency threshold: capital adequacy sensitivity

The third sensitivity desk evaluates the insurance-capital-implied solvency threshold beneath various:

- Insurance coverage protection ratio, starting from 3% to 7% of excellent funded publicity.

- Collateral recognition fee, starting from 30% to 70% of staked CHIP.

This desk behaves essentially in a different way from the buyback sensitivities. Increased protection necessities or decrease recognition charges improve the quantity of capital the system should supply, elevating the implied solvency threshold required for CHIP to credibly operate as backstop capital. Conversely, improved recognition or lowered protection compress the implied threshold even in stronger working eventualities.

This sensitivity explains why the insurance-implied solvency threshold can decline in bull instances. That consequence sometimes displays improved capital effectivity somewhat than weaker fundamentals, as much less backstop capital is required per unit of publicity.

Taken collectively, the sensitivity tables reinforce that CHIP’s valuation is constrained first by execution and mechanism design, and solely secondarily by market pricing assumptions. Market multiples matter, however solely after origination throughput, funding realization, governance capital coverage, and insurance coverage mechanics are credible.

The tables proven above mirror base-case assumptions. The complete valuation mannequin contains parallel sensitivity analyses for the bear and bull eventualities utilizing scenario-specific inputs.

Dangers

USD.AI operates on the intersection of onchain capital markets and real-world AI infrastructure finance. The first dangers are execution, margin, liquidity design, governance credibility, insurance coverage adequacy, authorized enforceability, focus, and macro funding circumstances.

The central working threat is whether or not the $1.5 billion marketed pipeline converts into funded originations on predictable timelines. Key constraints embrace:

- {Hardware} cargo and set up delays

- Underwriting and authorized settlement throughput

- Borrower deployment readiness

- Coordination throughout distributors, insurers, and custodians

As a result of protocol economics are pushed by funded quantity somewhat than signed pipeline, persistent delays would suppress charge era, publicity development, and web curiosity earnings. Upside eventualities are extremely delicate to funding realization.

Origination charges, servicing economics, and web curiosity unfold might compress as extra capital targets AI infrastructure lending. Aggressive borrower pricing or structurally greater depositor yields would scale back working surplus even when origination quantity grows. Since buyback-supported worth scales with distributable surplus, margin compression immediately pressures upside outcomes even in sturdy adoption eventualities.

USD.AI depends on QEV to handle redemptions in opposition to long-dated, illiquid collateral. The related threat is efficiency beneath stress. Potential failure modes embrace adversarial choice in redemption timing, redemption clustering throughout macro or sector shocks, and mispricing of queue precedence. If redemptions can’t be cleared predictably, sUSDai confidence may weaken, growing funding prices or forcing extra conservative system parameters that cut back capital effectivity.

CHIP’s worth accrual is governance-contingent somewhat than mechanically enforced. Even when governance authority is actual, the market won’t worth hypothetical surplus seize until there’s credible, repeated execution of tokenholder-aligned capital insurance policies, resembling buybacks, charge routing, or insurance-module incentives.

This creates two associated dangers: (1) governance might select to prioritize reinvestment, development, or threat buffers over tokenholder returns for prolonged durations, or (2) governance actions could also be episodic, inconsistent, or poorly executed, lowering market confidence in future worth accrual.

This uncertainty reinforces why our framework explicitly separates the implied solvency constraint from governance-contingent upside, somewhat than mixing them.

The insurance coverage module is a central pillar of USD.AI’s credit score structuring and risk-transfer framework. Nonetheless, the effectiveness of this construction will depend on adequate staking participation, lifelike collateral recognition of staked CHIP, and sustained confidence within the insurance coverage mechanism throughout stress occasions.

If protection proves insufficient, or if staked CHIP shouldn’t be perceived as credible backstop capital, the protocol might have to extend protection ratios, elevate incentives, or constrain development. These changes would improve capital depth and alter the solvency threshold required to keep up ample protection.

CALIBER is positioned as a authorized and technical framework for tokenizing GPU {hardware} into enforceable onchain collateral. At scale, this exposes USD.AI to regulatory, jurisdictional, and enforcement threat, together with mismatches between onchain representations and offchain authorized claims, custody or insurance coverage disputes, and regulatory modifications affecting asset tokenization, secured lending, or stablecoin-denominated credit score. Any breakdown in authorized enforceability would undermine collateral credibility, impair restoration in default eventualities, and improve required threat buffers throughout the system.

Early GPU infrastructure finance is prone to exhibit borrower, vendor, and geography focus, notably round giant services or marquee counterparties. Focus will increase tail threat from idiosyncratic failures, operational disruptions, or regulatory actions affecting particular counterparties or areas. Whereas diversification might enhance over time, early-stage focus may amplify volatility in originations, defaults, and insurance coverage outcomes relative to modeled averages.

Lastly, USD.AI is uncovered to broader macro and crypto market cycles. Intervals of threat aversion, stablecoin contraction, or onchain liquidity stress may cut back out there funding even when borrower demand stays intact. As a result of USD.AI monetizes credit score circulate and publicity, not simply balances, extended capital market disruptions would immediately impair throughput and income era.

Closing Ideas

USD.AI is trying to construct onchain credit score infrastructure for one of the crucial capital-intensive markets, real-world AI compute deployment. Its core wager shouldn’t be that demand for GPUs exists, however that this demand might be transformed right into a scalable, legally enforceable collateral and funding pipeline that onchain capital markets can underwrite. If profitable, USD.AI would characterize a significant step towards bridging DeFi liquidity with productive, non-crypto collateral.

The protocol’s differentiation is structural. CALIBER is meant to make bodily GPU collateral enforceable and verifiable, whereas QEV is designed to handle redemption stress in opposition to long-dated, illiquid belongings by queue-based pricing somewhat than pressured liquidity. This structure is directionally according to the realities of infrastructure finance, however it additionally concentrates execution threat.

CHIP is greatest understood as a governance and risk-policy asset working throughout two distinct financial mechanisms. The excess-driven pathway will depend on governance allocating distributable surplus towards buybacks and sustaining that coverage over time. Individually, the insurance-capital-implied solvency threshold displays the capitalization required if CHIP is relied upon as acknowledged backstop capital inside the protocol’s protection framework, the place required protection ratios and collateral recognition effectivity decide capital depth. Underneath our modeled eventualities, buyback-supported FDVs vary from $46.4 million (bear) to $329.6 million (base) and $1.74 billion (bull). The insurance-capital-implied solvency thresholds vary from $270.1 million (bear) to $275.6 million (base) and $503.2 million (bull).

Finally, the funding query is whether or not USD.AI can constantly convert pipeline into funded originations at scale whereas sustaining capital effectivity and system stability, and whether or not governance establishes a repeatable, market-credible mechanism for CHIP worth accrual. If funding realization improves, liquidity design performs as supposed, and governance demonstrates disciplined capital coverage, USD.AI can evolve into sturdy credit score infrastructure with defensible economics. If execution latency persists, spreads compress earlier than scale is reached, or governance worth accrual stays aspirational somewhat than observable, CHIP’s upside case can be tough for markets to underwrite no matter AI infrastructure demand.