By Marc Kavinsky, Lead Editor at IoT Business News.

According to Omdia, cellular IoT connections are projected to hit 5.9 billion by 2035, with NB-IoT, 5G Massive IoT, and eRedCap driving the upcoming wave of growth in both modules and connections.

The cellular IoT landscape is no longer following a single evolutionary path. For hardware manufacturers and connectivity suppliers, the coming decade is expected to be shaped less by a broad shift to 5G and more by a diversified blend of technologies, where factors like cost, power efficiency, network rollout status, and specific application needs determine which radio standard prevails in each scenario.

This is the central takeaway from a fresh Omdia study, which projects that cellular IoT connections will climb to 5.9 billion by 2035. The research organization pinpoints three technological pillars as critical to that expansion: 5G RedCap and eRedCap, 5G Massive IoT, and 4G LTE Cat-1bis modules.

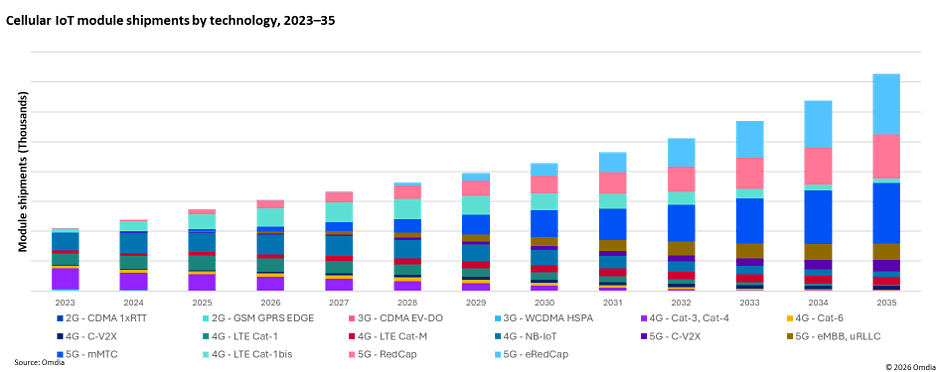

What stands out about this projection is not merely the overall growth number. Omdia is highlighting a cellular IoT arena that remains highly varied, rather than one where 5G simply supplants older standards in a straightforward progression. By 2035, NB-IoT, mMTC, and eRedCap are anticipated to make up 65% of all cellular IoT connections, underscoring the enduring significance of low-power, lower-complexity connectivity options alongside more advanced 5G alternatives.

eRedCap reshapes the RedCap outlook

Among the more pointed findings in Omdia’s assessment is the expectation that eRedCap will outperform standard RedCap in market uptake. This difference is significant. RedCap was originally created to fill the gap between premium 5G broadband devices and low-power IoT endpoints, but Omdia observes that its uptake has been held back by steep module costs and slower-than-expected 5G Standalone network deployments.

eRedCap, on the other hand, arrives under more favorable circumstances. Omdia reports that the first eRedCap module rollouts have already occurred in 2026, and the technology stands to gain from the expanding availability of 5G SA networks. In practical terms, this means eRedCap is likely to encounter fewer of the timing and infrastructure hurdles that hampered early RedCap implementations.

This is where the analysis diverges from many other cellular IoT projections: it does not lump all 5G IoT into one bucket. Rather, it carves out separate roles for RedCap, eRedCap, Massive IoT, NB-IoT, LTE-M, and Cat-1bis. For original equipment manufacturers, this distinction carries real operational weight because the choice of module directly influences product pricing, certification efforts, power consumption targets, roaming capabilities, and lifecycle management strategies.

Omdia also points out that RedCap has gathered some momentum over the past year following the release of the newest Apple Watch lineup featuring RedCap technology. Although wearables occupy a different segment than industrial sensors or utility equipment, the integration of RedCap into a mass-market consumer device can lend credibility to the broader technology ecosystem spanning chipsets, modules, and carrier support.

Regional patterns continue to diverge

NB-IoT remains overwhelmingly concentrated in Asia and Oceania, which together represented 86% of worldwide NB-IoT module shipments in 2025, per Omdia’s data. LTE-M, by contrast, is seeing broader global traction, with Asia and Oceania expected to account for 58% of module market share by 2035.

For international device makers, this geographic imbalance presents a tangible engineering challenge. A product destined for multiple regions may require different module configurations, fallback protocols, or connectivity profiles based on where it will ultimately be used. The forecast thus reinforces a well-known yet frequently overlooked reality: achieving scale in cellular IoT depends not only on network footprint but on aligning technology portfolios with the specific conditions faced by operators in each region.

Regulation is another force reshaping the landscape. Omdia calls attention to Europe’s Cyber Resilience Act, which requires products to be designed with built-in security and supported with vulnerability patches for five years, as a catalyst for structural transformation across the continent. The firm notes this is speeding up the shift toward eSIM, eUICC, and resilient SIM architectures. For manufacturers, this ties connectivity decisions more closely to long-term security upkeep and device administration, rather than viewing the SIM as nothing more than a provisioning tool.

In North America, Omdia cites the US Infrastructure Investment and Jobs Act and the Inflation Reduction Act as key enablers for deployments across smart grids, utility networks, and EV charging infrastructure. These are segments where ruggedized 4G and 5G modules are forecast to experience near-term demand, according to the research.

Automotive sector shifts toward cellular primacy

The automotive vertical is on track to surpass 1 billion cellular IoT connections by 2035. Omdia anticipates that 89% of automotive modules will rely on 5G technologies by that point, propelled by the adoption of connected vehicles among both Chinese and global carmakers and by the growing requirements for vehicle-to-everything communication.

For systems integrators and business buyers, the wider implication is that cellular IoT procurement is becoming increasingly tailored to specific applications. Utility companies, EV charging operators, fleet management platforms, automakers, and industrial equipment suppliers will not be making abstract choices between “4G” and “5G.” Instead, they will be evaluating NB-IoT, LTE-M, Cat-1bis, RedCap, and eRedCap against criteria such as deployment geography, anticipated device lifespan, regulatory security mandates, and the network infrastructure available on the ground.

Omdia’s projection therefore signals a broader ecosystem evolution: cellular IoT growth through 2035 will hinge on a wider array of purpose-optimized radio technologies rather than a single prevailing standard. This creates greater adaptability for the market, but also added complexity for OEMs and connectivity providers tasked with supporting products across extended lifecycles in inconsistent regional environments.